A cyberattack can happen to any business, regardless of size. We at Brooks Cannon Insurance Group see firsthand how quickly a data breach can drain resources and damage trust with customers.

Cyber liability insurance protects you when the worst happens. This guide walks you through what you need to know to keep your Dallas-area business safe.

The Real Cost of Cyberattacks on Your Business

Cyberattacks Hit Hard and Hit Often

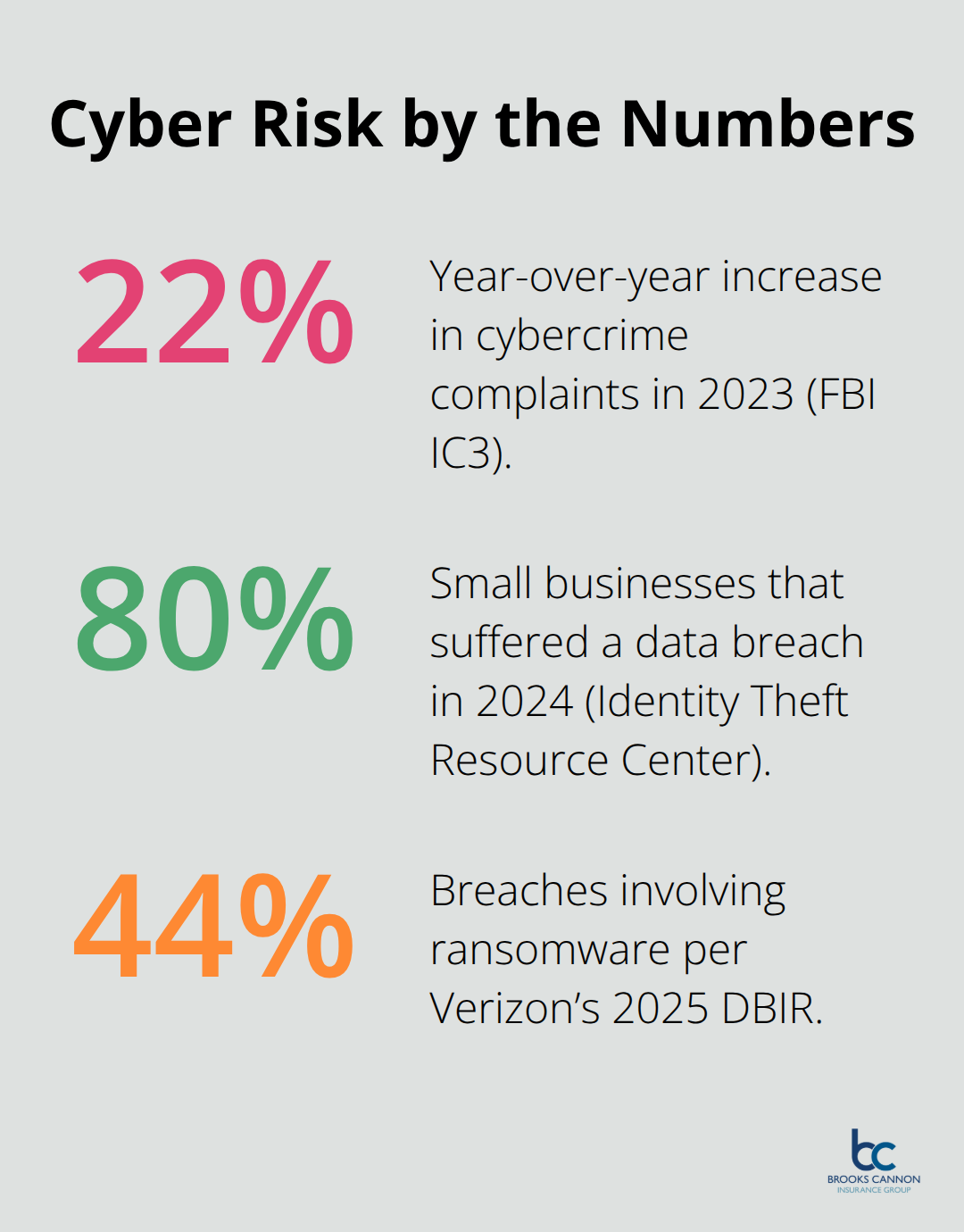

The numbers tell a sobering story. The FBI’s Internet Crime Complaint Center received over 880,000 cybercrime complaints in 2023 alone, with losses exceeding $12.5 billion. That represents a 22 percent year-over-year increase. For Dallas-area businesses, the threat is immediate and escalating. The Identity Theft Resource Center reported that 80 percent of small businesses suffered a data breach in 2024, with an average expense around $500,000 per incident. These are not hypothetical scenarios or worst-case outliers. These are real costs hitting real companies in your market right now.

The Price Tag Keeps Growing

Ransomware demands alone average around $1.1 million per incident in Texas, with some attacks demanding significantly more. Business Email Compromise attacks cost victims over $35,000 on average, while funds transfer fraud can drain nearly $185,000 per incident. The scope of attacks has expanded dramatically. Verizon’s 2025 Data Breach Investigations Report found that ransomware was involved in 44 percent of all breaches and accounted for 75 percent of system-intrusion breaches. Phishing attacks, which remain deceptively simple to execute, average nearly $100,000 in damages. Cloud collaboration tool exploits cost organizations about $300,000 on average.

What makes this worse is that small and mid-sized firms in the Dallas area are prime targets. Criminals use automation to cast wide nets, hitting smaller organizations that often lack sophisticated security infrastructure. The average global cost of a data breach reaches $4.8 million. Your reputation takes a hit alongside your finances. When customer data leaks, trust erodes. Detection and containment alone take approximately 280 days on average, during which your business continues to bleed money and credibility.

Your Industry Determines Your Risk Level

Different industries face wildly different threat levels, and your cyber liability insurance must reflect your specific risk. Healthcare organizations face relentless attacks because patient data commands high prices on the dark web. Financial institutions face sophisticated attacks aimed at stealing customer information and funds. Energy and infrastructure operators deal with nation-state-level threats. Even retail businesses that handle payment card data face significant exposure.

If you process credit cards, handle sensitive personal information, or use third-party applications to run operations, a breach is not a possibility but a probability. The question is whether you are financially prepared when it happens. Your industry exposure directly shapes the coverage you need and the limits you should carry. Understanding where your business sits on the threat spectrum is the first step toward adequate protection.

What Cyber Liability Insurance Actually Covers

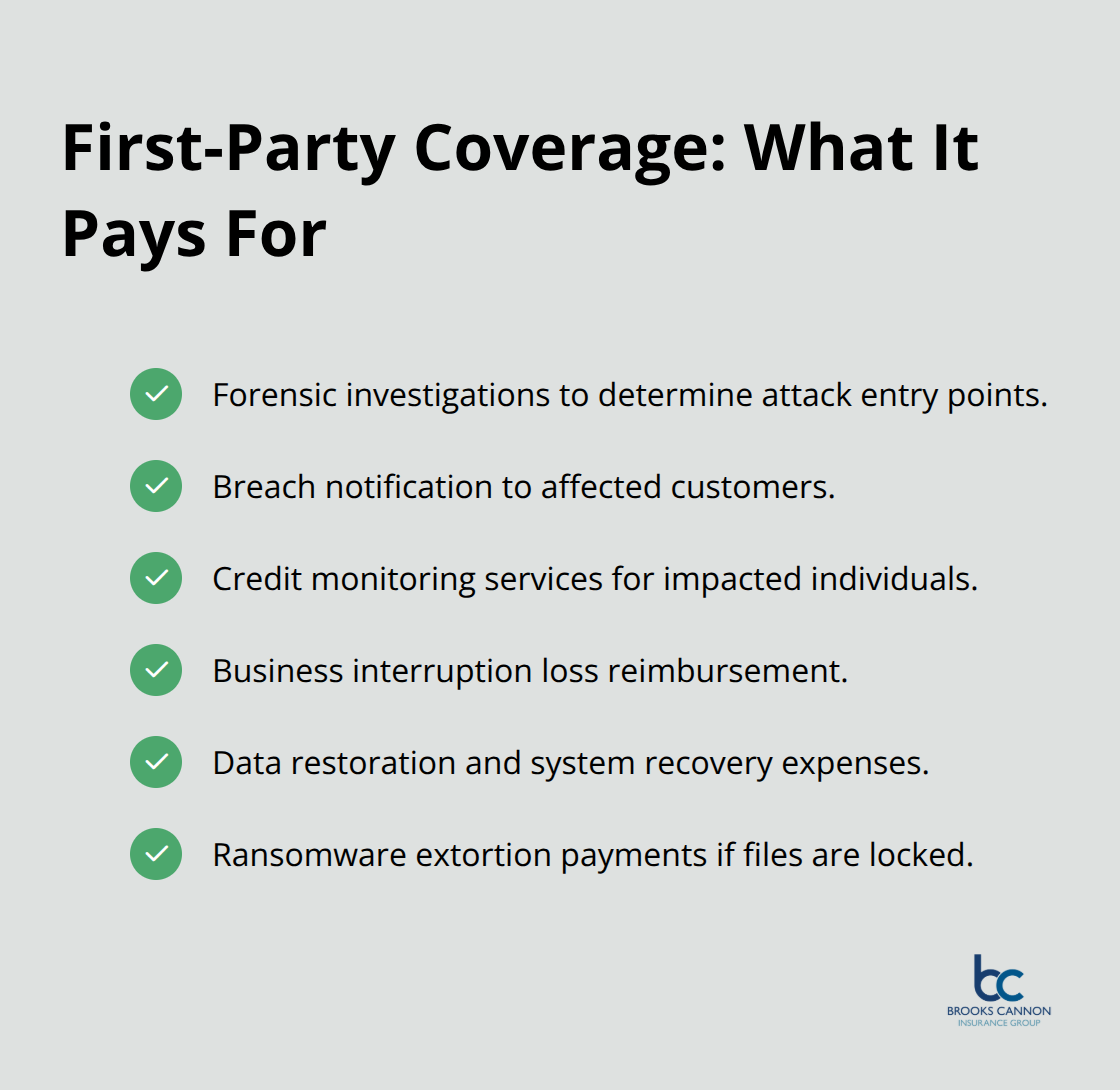

First-Party Coverage: Protecting Your Direct Costs

Cyber liability insurance splits into two distinct layers: first-party coverage and third-party coverage. First-party coverage pays for costs your business directly incurs when a breach happens. This includes forensic investigations to determine how attackers entered your systems, notification costs to inform affected customers, credit monitoring services you must offer to victims, business interruption losses when your network goes down, data restoration and system recovery expenses, and ransomware extortion payments if criminals lock your files.

Willis Towers Watson’s analysis of cyber claims from 2013 through 2019 found that data breach response and crisis management represented about 73 percent of all claims. This statistic underscores how frequently businesses tap first-party coverage when incidents occur. The average breach investigation alone costs around $58,000, a single expense that justifies carrying cyber insurance on its own.

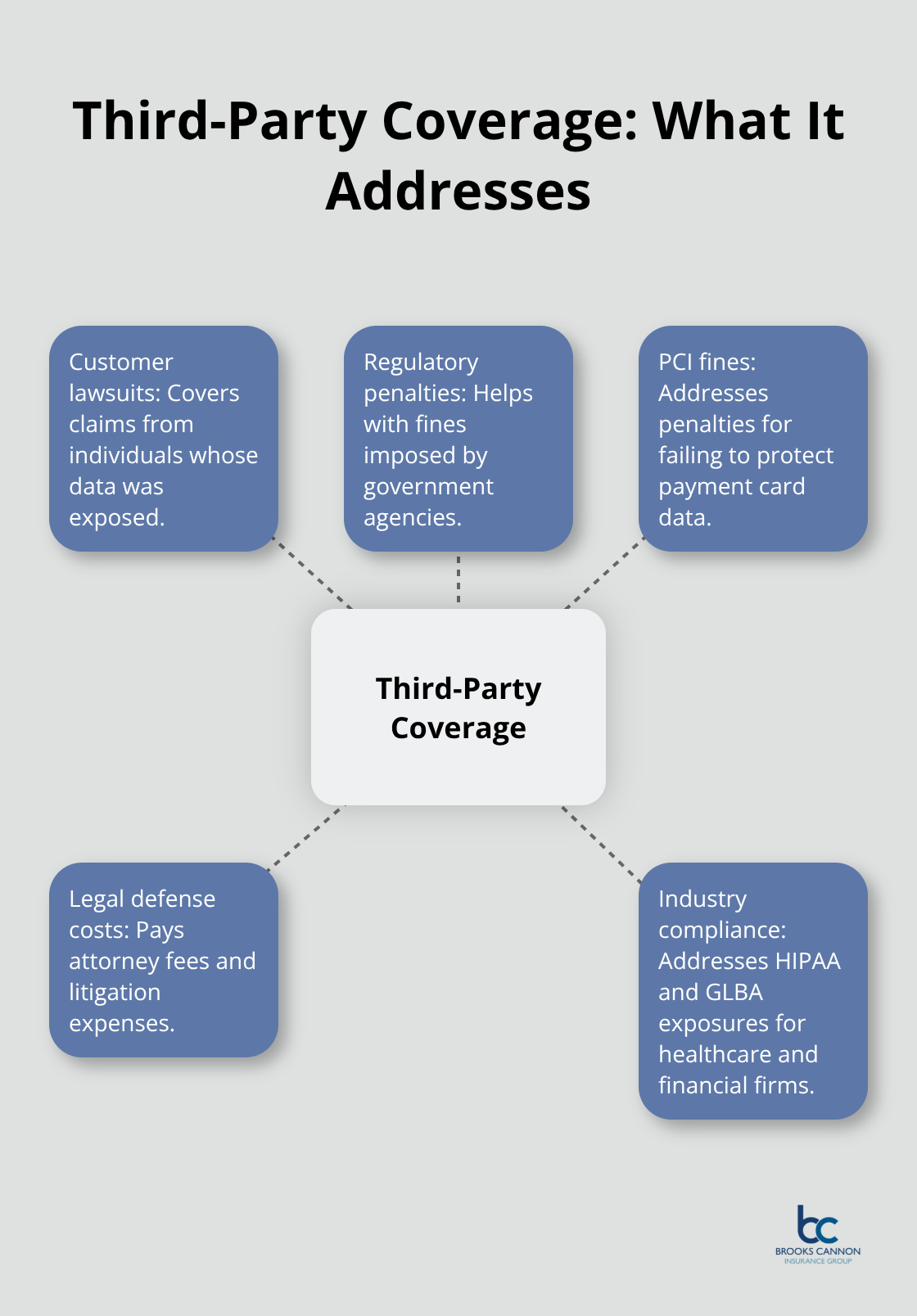

Third-Party Coverage: Handling Liability from Others

Third-party coverage handles liabilities arising from how the breach affects others. This protects you against lawsuits from customers whose data leaked, regulatory penalties imposed by government agencies, PCI fines if you fail to protect payment card information, and legal defense costs. For healthcare organizations in the Dallas area subject to HIPAA rules, third-party coverage can reimburse certain regulatory penalties when patient data is compromised. Financial institutions face similar exposure under GLBA compliance requirements. If your business holds customer information, you face genuine third-party liability when that data reaches the wrong hands.

Why General Liability Falls Short

The practical reality separates cyber insurance from general liability coverage. A standard commercial general liability policy does not cover data breaches, network security failures, or cyber extortion demands. You need dedicated cyber liability coverage to address these exposures. A comprehensive cyber policy typically costs between $100 and $200 monthly for small businesses, though premiums vary significantly based on your industry, revenue, security practices, and coverage limits.

Strong security measures like multi-factor authentication and data encryption can lower premiums by 10 to 20 percent, creating a direct financial incentive to strengthen your defenses. In Texas, where ransomware demands average $1.1 million per incident, business interruption coverage becomes non-negotiable for companies that depend on continuous network access.

Contractual Requirements Drive Coverage Decisions

If you operate in healthcare, finance, energy, or handle payment processing, your contracts likely already require cyber liability coverage with minimum limits. Reviewing your vendor agreements and client contracts for cyber insurance clauses should happen immediately if you have not done so already. Government agencies, healthcare networks, lenders, and energy operators frequently mandate minimum coverage limits before they work with you. These contractual obligations often exceed what you might otherwise purchase, making policy review a business necessity rather than an optional exercise.

Finding the Right Coverage Limits for Your Business

Calculate Your Actual Data Exposure and Breach Costs

Start by calculating exactly how much data your business holds and how much an incident would cost to remediate. Pull your vendor contracts immediately and search for cyber insurance clauses. Government agencies, healthcare networks, lenders, and energy operators in Texas frequently mandate minimum coverage limits before they work with you. If a contract requires $2 million in coverage, that becomes your floor, not a suggestion. This contractual obligation often exceeds what you might otherwise purchase, making policy review a business necessity rather than an optional exercise.

Match Coverage Limits to Your Business Size and Industry

Small businesses typically qualify for policies with limits between $1 million and $5 million, with annual premiums ranging from $500 to $2,500 and deductibles as low as $1,000. Mid-sized firms usually carry $5 million to $25 million in coverage with annual costs between $2,500 and $15,000 and deductibles up to $25,000. The gap between these tiers matters because a $1 million limit sounds substantial until you face a $4.8 million average breach cost.

Your industry determines your actual exposure. Healthcare organizations need coverage that specifically addresses HIPAA penalties. Financial institutions need limits that account for GLBA compliance risks and potential PCI fines reaching $750,000 for payment data breaches. Energy operators increasingly face contractual requirements anticipating federal reporting rules. A Dallas-area business processing credit cards should carry minimum limits substantially higher than a professional services firm that stores no payment data.

Optimize Your Deductible and Premium Balance

Your deductible choice directly impacts your monthly premium. Lower deductibles cost more monthly but reduce your out-of-pocket exposure when a breach happens. Most small businesses select deductibles between $1,000 and $5,000 as a practical balance. Strong security practices matter financially. Implementing multi-factor authentication, enforcing strong password policies or passkeys, and encrypting sensitive data can reduce your premiums by 10 to 20 percent. Insurers view these controls as genuine risk reduction, not compliance theater.

Review Exclusions and Verify Essential Coverages

Review policy exclusions before signing any agreement because standard cyber liability policies often exclude gaps in general liability, employment practices liability, or professional liability coverage. Known vulnerabilities and outdated systems frequently trigger coverage denials. If your business runs legacy software that your IT team has flagged as vulnerable, an insurer will likely exclude coverage for breaches exploiting that weakness.

Ransomware coverage should be explicitly included and specify whether extortion payments are covered. Business interruption coverage needs clear language defining what constitutes a covered outage and how lost income gets calculated. Crisis management and breach notification coverage should include costs for forensic investigations, customer notification, credit monitoring services, and regulatory defense. Third-party coverage protecting you against lawsuits and regulatory penalties requires careful review. If you work with government agencies or handle healthcare data, verify that regulatory defense and penalty coverage align with your actual exposure.

Add Endorsements for Your Specific Threats

Additional endorsements address specific risks and strengthen your protection. Cloud misconfigurations frequently expose data, particularly for startups and SaaS firms, so if your business relies heavily on cloud infrastructure, endorsements covering cloud-specific incidents become essential. Funds transfer fraud coverage protects against deceptive wire transfer schemes. Business email compromise coverage addresses a threat that costs victims over $35,000 on average per incident. A cyber risk assessment before purchasing coverage identifies your specific exposures and ensures your policy actually matches your business. A tailored quote based on your actual operations costs less than guessing at coverage limits and discovering gaps after a breach occurs.

Final Thoughts

Cyber liability insurance protects your Dallas-area business when a breach strikes, not if it strikes. The data confirms this reality: 80 percent of small businesses suffered a data breach in 2024, with average costs around $500,000 per incident, while ransomware demands in Texas average $1.1 million and Business Email Compromise attacks drain $35,000 on average. These incidents happen to real companies right now, and without proper coverage, a single attack forces you to choose between paying for recovery or closing your doors.

When a breach occurs, cyber liability insurance coordinates forensic investigations, legal defense, regulatory compliance, and customer notification so your business receives professional guidance during the most stressful moment. For healthcare organizations facing HIPAA penalties, financial institutions managing GLBA compliance, and any business handling payment card data, cyber liability insurance addresses contractual requirements that your clients and partners already demand. Strong security practices like multi-factor authentication and data encryption reduce your risk and lower your premiums by 10 to 20 percent, creating genuine protection that insurance then backs up financially.

We at Brooks Cannon Insurance Group work with top-rated carriers to find cyber liability coverage that matches your actual exposure and budget. Our licensed experts review your contracts, assess your data handling practices, and recommend coverage limits that protect your business without overpaying for unnecessary protection. Contact us today to discuss your cyber liability insurance needs and get a tailored quote based on your specific situation.