Cyberattacks hit businesses every 39 seconds, making data breach insurance more important than ever. The average cost of a data breach reached $4.45 million in 2023, according to IBM’s Cost of a Data Breach Report.

We at Brooks Cannon Insurance Group see firsthand how cyber incidents can devastate unprepared businesses. Smart coverage protects your company’s finances and reputation when hackers strike.

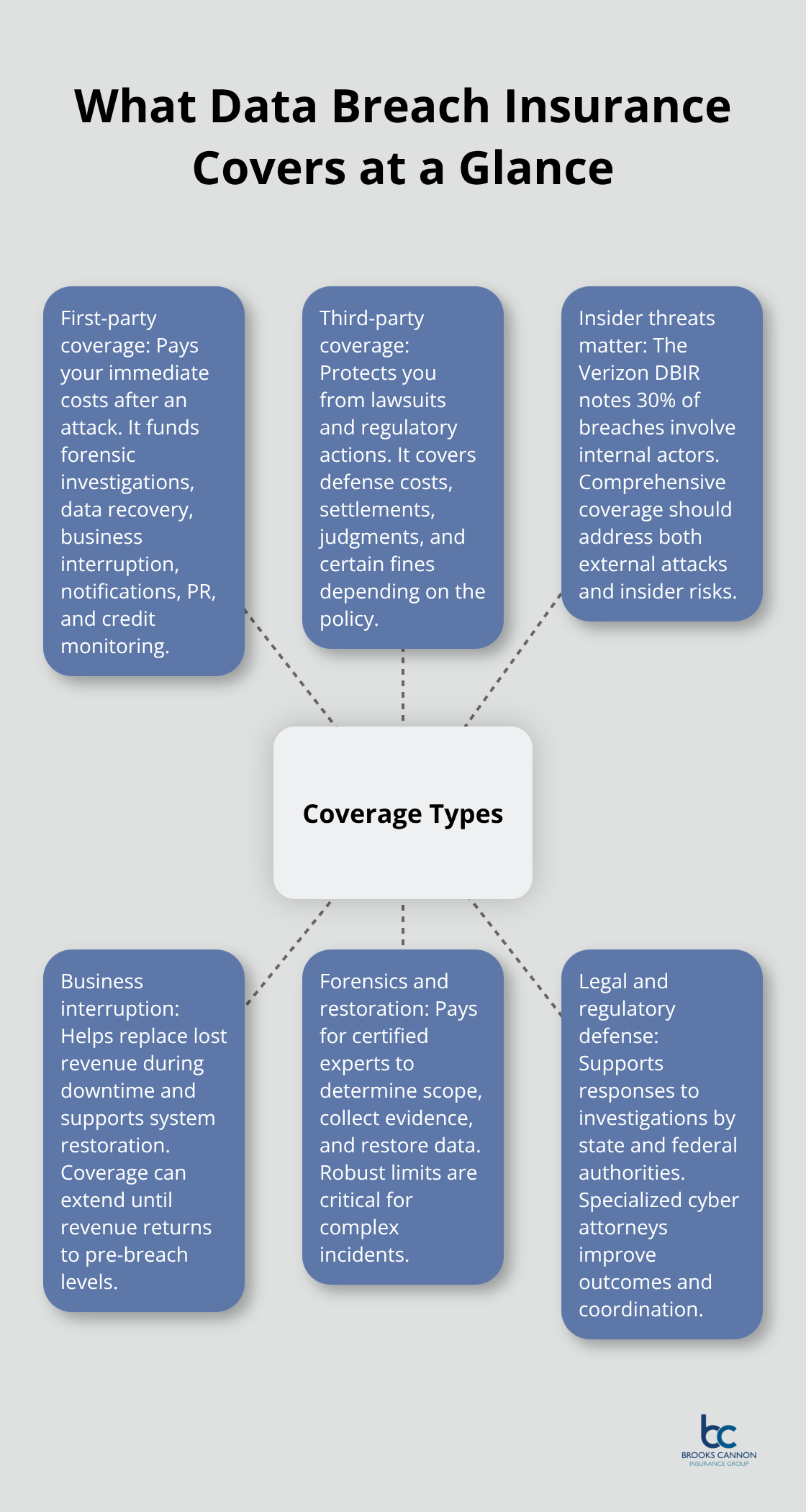

What Data Breach Insurance Actually Covers

Data breach insurance divides into two distinct coverage types that address different financial exposures. First-party coverage handles your direct losses when attackers compromise your systems. This includes forensic investigations, data restoration costs, business interruption expenses, and notification requirements. Third-party coverage protects against lawsuits and regulatory actions from affected customers or partners.

The Verizon Data Breach Investigations Report shows 30% of breaches involve internal actors, which makes comprehensive coverage vital for both external attacks and insider threats.

First-Party Protection Covers Your Immediate Costs

When hackers strike, first-party coverage pays for incident response teams (typically $15,000 to $50,000 for small businesses according to recent industry data). This coverage includes forensic investigations to determine breach scope, data recovery services, and mandatory customer notifications. Business interruption protection covers lost revenue during system downtime, which averaged 287 days for ransomware attacks in 2023 based on IBM research. Credit monitoring services for affected customers, public relations campaigns to protect reputation, and regulatory compliance costs also fall under first-party protection.

Third-Party Coverage Shields Against Legal Claims

Third-party coverage activates when customers, partners, or vendors sue your business after a data breach. This protection covers defense costs, settlements, and judgments from privacy violation lawsuits. Regulatory fines from state attorneys general or federal agencies also trigger third-party coverage. 88% of breaches stem from human error, which makes robust liability protection essential. Policy limits typically range from $1 million to $10 million, with deductibles between $10,000 and $100,000 (depending on business size and risk profile).

The next consideration involves understanding why these coverage types have become essential for modern businesses facing escalated cyber threats.

Why Data Breach Protection Has Become Non-Negotiable

Cybercrime costs are projected to reach $15.63 trillion by 2029 according to Statista. Ransomware payments alone surged from $567 million in 2022 to $1.1 billion in 2023 based on Chainalysis data. These numbers show cyber incidents drain company coffers faster than traditional risks. Small businesses face average breach costs of $165,000, while larger companies pay millions in recovery expenses. Business email compromise scams cost victims $3 billion in 2023, affecting 22,000 companies globally according to Symantec research.

Regulatory Penalties Strike Hard Without Warning

Texas businesses must comply with state breach notification laws that require customer alerts within 60 days of discovery. Federal regulations like HIPAA impose fines up to $1.5 million per incident for healthcare providers. The Payment Card Industry Data Security Standard mandates specific protections for credit card data, with violations that trigger fines between $5,000 and $100,000 monthly. California’s Consumer Privacy Act affects any business that serves California residents, which creates liability exposure beyond state borders. Companies that handle European customer data face GDPR fines that reach 4% of annual revenue.

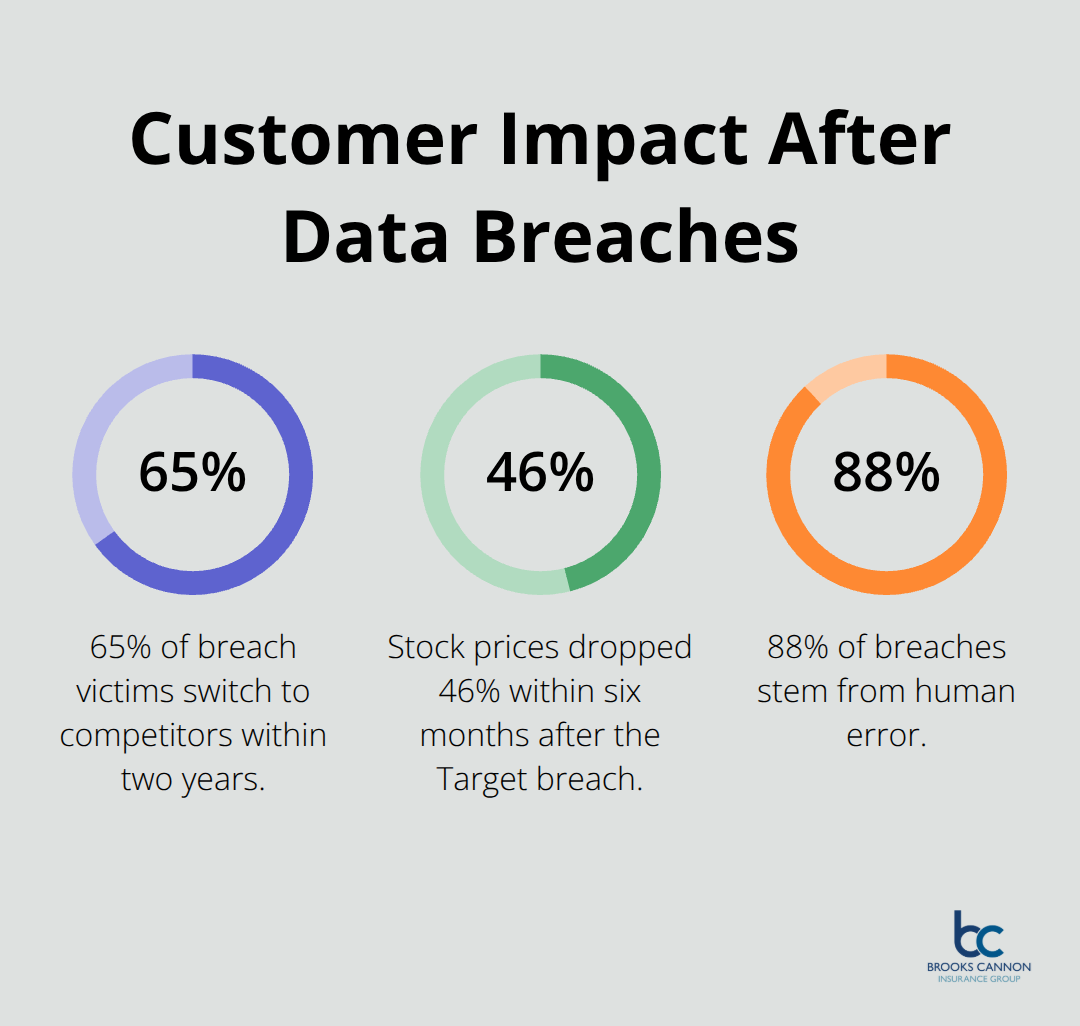

Customer Trust Vanishes After Security Failures

Target lost 70 million customers after their 2013 breach, with stock prices that dropped 46% within six months. Equifax faced a $700 million settlement and permanent reputation damage after their 2017 incident affected 147 million Americans. Studies show 65% of breach victims switch to competitors within two years. Customer acquisition costs increase 200% for breached companies as prospects avoid businesses with security problems.

Public relations campaigns cost $50,000 to $500,000 (depending on breach scope), which makes reputation recovery expensive and uncertain.

Supply Chain Attacks Create Hidden Vulnerabilities

Supply chain attacks doubled in 2023 compared to the previous three years, costing businesses $45.8 billion according to Juniper Research. These incidents target vendors and partners to access primary targets through trusted relationships. The SolarWinds attack affected 18,000 organizations through a single compromised software update. Companies now face liability for third-party breaches that compromise their customer data through vendor relationships.

Smart businesses recognize these escalated risks and seek comprehensive protection through specialized insurance policies that address modern cyber threats.

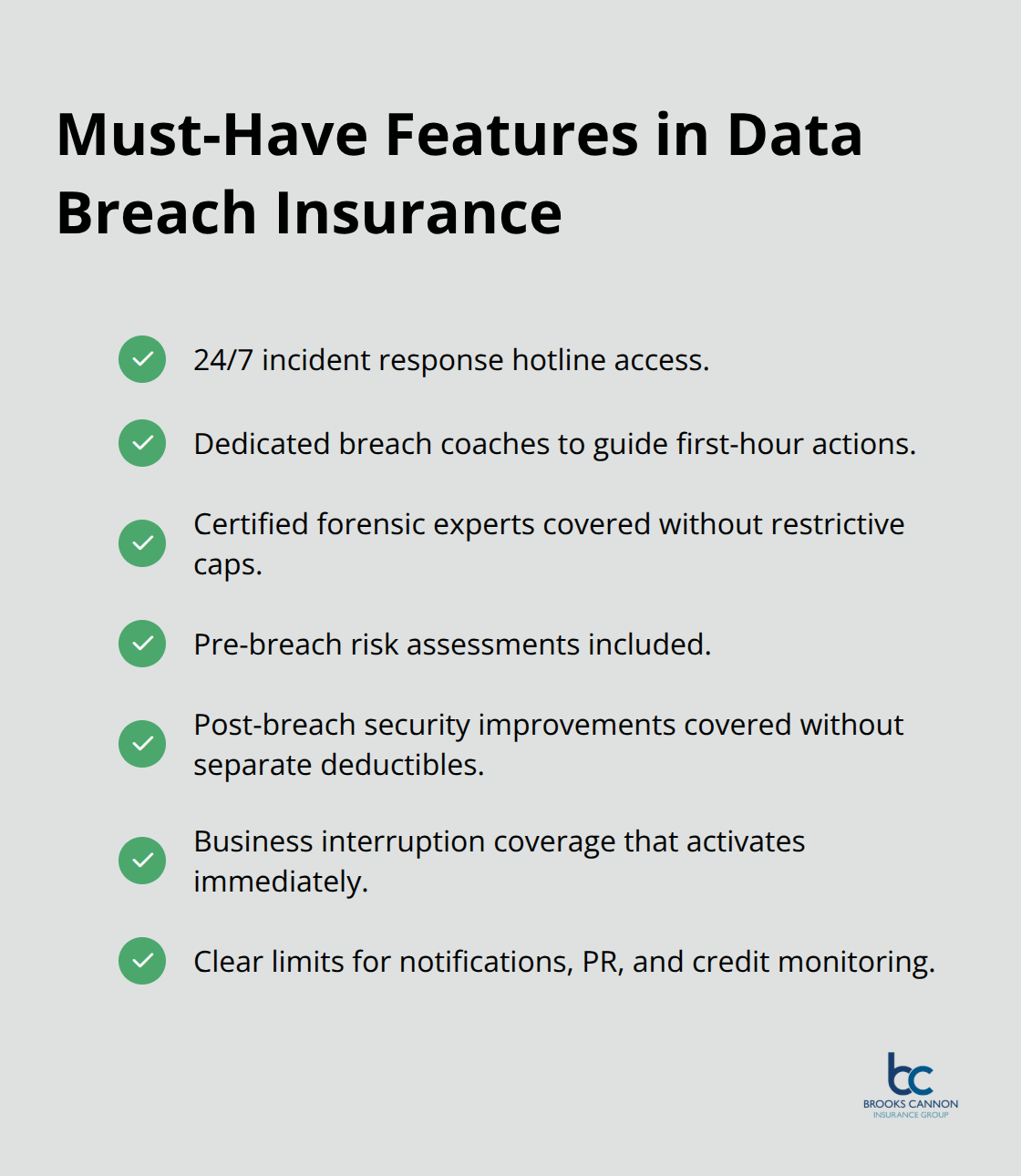

Key Features to Look for in Data Breach Policies

Data breach policies vary dramatically in coverage quality, making feature selection the difference between financial protection and bankruptcy. Incident response coverage should include 24/7 hotlines with dedicated breach coaches who guide you through the first critical hours. Forensic investigation coverage must pay for certified experts who determine breach scope and preserve evidence for legal proceedings. The best policies cover pre-breach risk assessments and post-breach security improvements without separate deductibles.

Avoid policies that cap forensic costs below $100,000, as complex investigations often exceed this amount according to recent industry claims data.

Legal Defense Coverage Protects Against Multiple Threats

Strong policies cover regulatory investigations from state attorneys general, federal agencies, and industry bodies without shared limits. Defense coverage should include specialized cyber attorneys rather than general business lawyers who lack breach experience. Regulatory fine coverage varies significantly between carriers, with some that exclude government penalties entirely while others provide dedicated sublimits up to $5 million. Regulatory agencies continue to impose significant privacy-related penalties on businesses that fail to protect customer data. Class action lawsuit coverage requires separate consideration, as these claims often exceed standard liability limits and create prolonged legal expenses.

Business Interruption Protection Addresses Revenue Loss

Revenue loss coverage should activate immediately when systems go offline, not after wait periods that delay payments. The strongest policies cover dependent business income when suppliers or customers suffer breaches that disrupt your operations. System restoration coverage must include both hardware replacement and software license costs, which can reach substantial amounts per incident based on industry research. Extended period coverage continues payments beyond system restoration until revenue returns to pre-breach levels. Avoid policies that exclude cloud service outages, as many companies experience third-party cyber incidents according to industry data.

Incident Response and Forensic Investigation Coverage

Quality policies provide immediate access to incident response teams with proven track records in breach management. These teams coordinate with law enforcement, manage media relations, and handle customer notifications within regulatory timeframes. Forensic investigation coverage should pay for digital evidence collection, malware analysis, and vulnerability assessments that identify attack vectors. The best policies cover both internal IT staff overtime and external consultant fees during incident response. Network security monitoring services help detect future attacks and often reduce premium costs through risk mitigation credits.

Final Thoughts

Data breach insurance has transformed from optional coverage to business necessity as cyber threats multiply and regulatory penalties intensify. The projected $15.63 trillion cybercrime cost by 2029 makes comprehensive protection mandatory for companies that handle sensitive information. Smart businesses recognize these escalated risks and act decisively to protect their operations.

Proper coverage selection requires careful evaluation of your specific risk profile and regulatory requirements. Compare incident response capabilities, forensic investigation limits, and business interruption terms across multiple carriers. Review policy exclusions carefully, as coverage gaps can expose you during critical moments when protection matters most.

Independent agents access multiple carriers and negotiate terms that match your unique exposures (without the conflicts that captive agents face). We at Brooks Cannon Insurance Group help Dallas businesses navigate complex cyber insurance markets and secure appropriate protection levels. The cyber threat landscape continues to evolve, which makes regular policy reviews essential for maintaining adequate coverage as your business grows.