Luxury homes in Texas face unique risks that standard homeowners policies simply can’t handle. From severe weather events to high-value personal collections, these properties need specialized protection.

At Brooks Cannon Insurance Group, we help Dallas-area homeowners navigate the complexities of high value home insurance in Texas. The right coverage protects both your investment and your lifestyle.

Understanding High Value Home Insurance in Texas

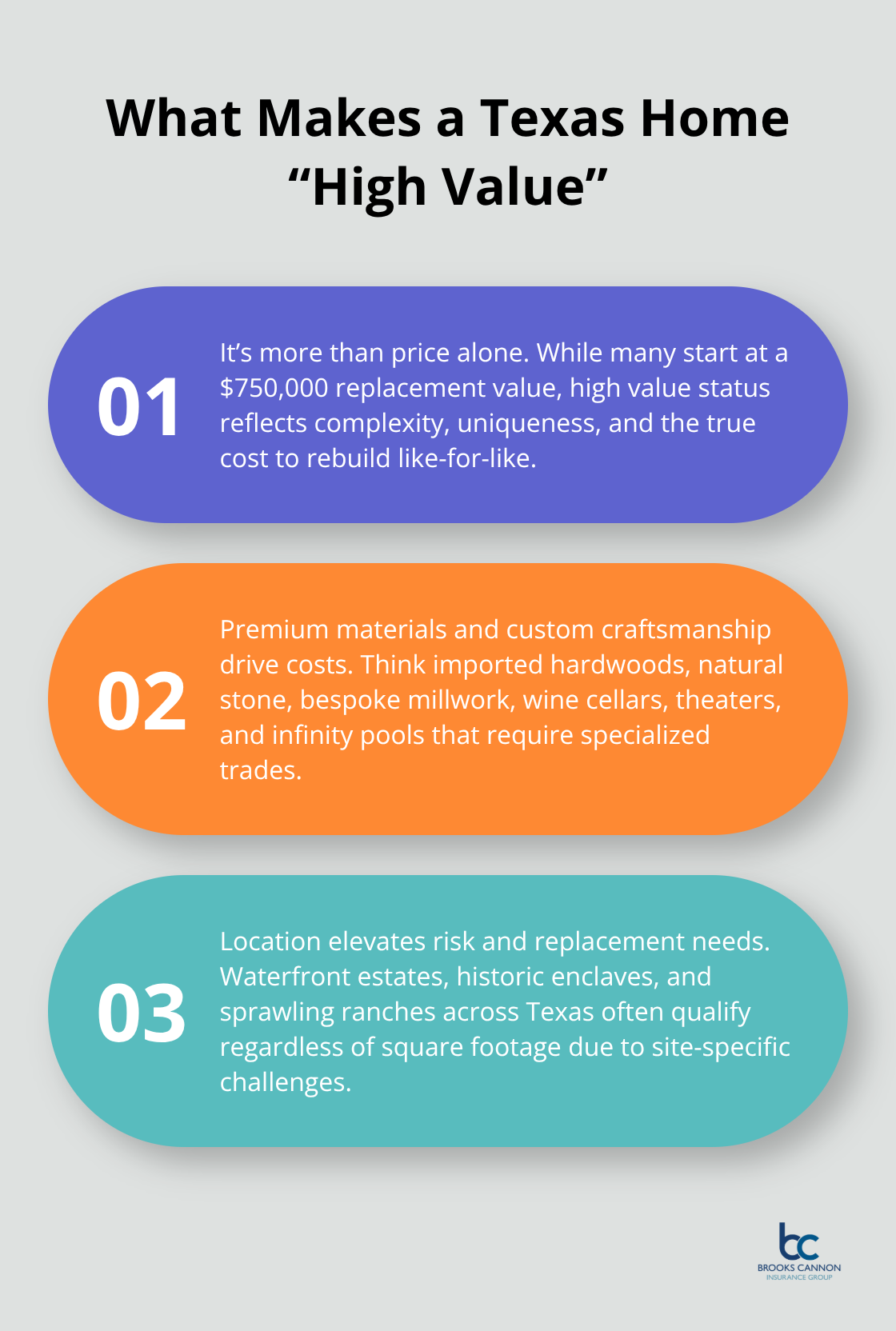

What Qualifies as a High Value Home in Texas

High value homes in Texas start at replacement values of $750,000, but the definition extends far beyond dollar amounts. These properties feature custom architectural details, premium materials like natural stone or imported hardwood, and luxury amenities such as wine cellars, home theaters, or infinity pools. Location plays a major role – waterfront estates in Lake Travis, historic mansions in Highland Park, or ranch properties in Hill Country all qualify regardless of square footage.

Standard Insurance Fails Luxury Properties

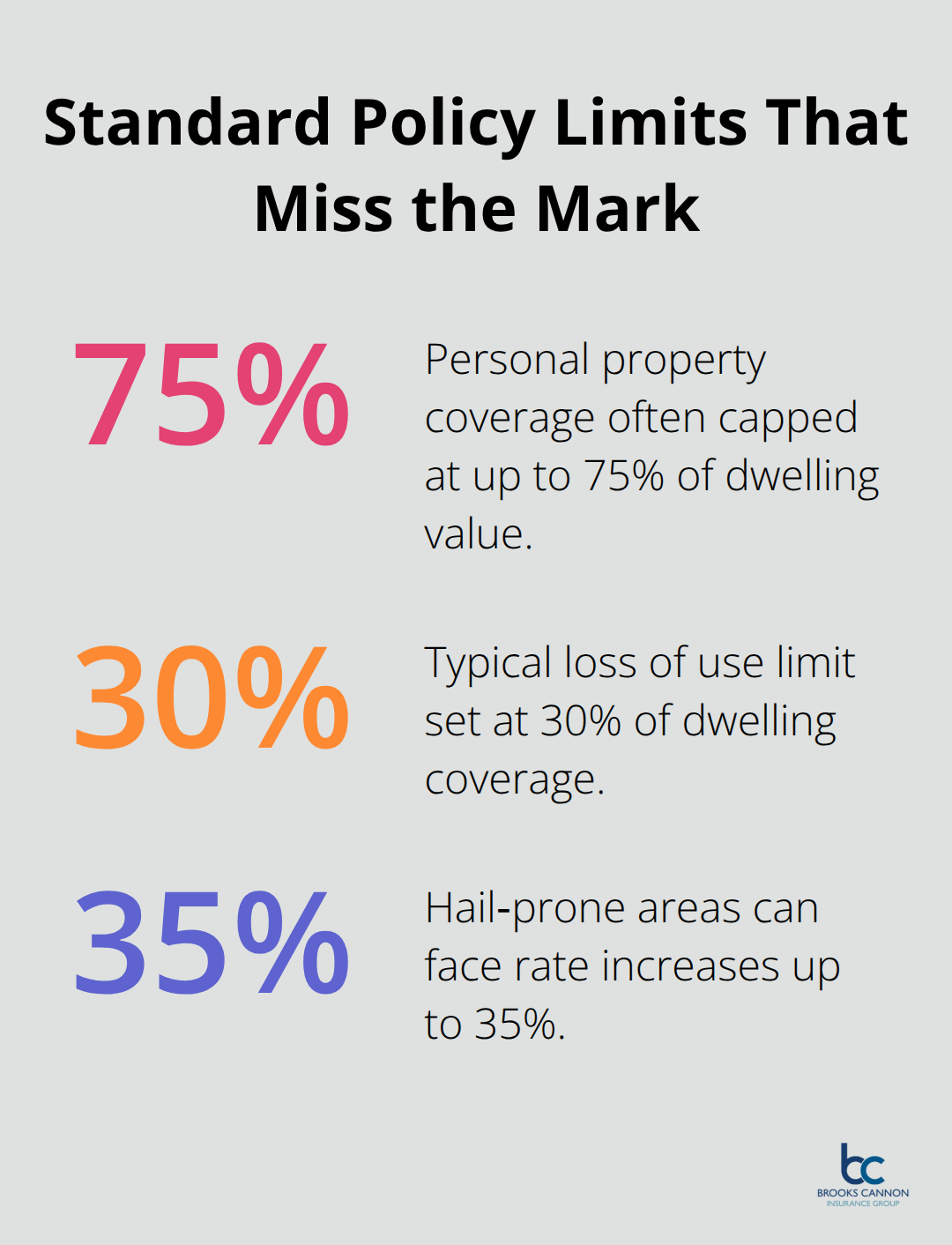

Traditional H03 homeowners policies cap personal property coverage at 50-75% of the home value and impose strict sub-limits on valuables. A standard policy might limit jewelry to $2,500 total, while luxury homeowners often own pieces worth $50,000 or more. Standard policies also use actual cash value settlements for older items, which means your 10-year-old custom kitchen receives depreciated value, not replacement cost. High value policies eliminate these restrictions and offer agreed value coverage that pays full replacement cost without depreciation disputes.

Texas Weather Requires Specialized Protection

Texas faces unique weather risks that luxury homeowners must address through specialized coverage. The Texas Department of Insurance actively monitors property damage claims across the state. High value policies offer extended replacement cost coverage of 125-150% above home limits, which protects against post-storm construction cost spikes. Wind and hail deductibles often apply separately from other perils, and luxury policies can reduce these to flat dollar amounts rather than percentage-based deductibles that could reach $25,000 on a $2.5 million home.

The right high value policy addresses these Texas-specific challenges while providing the comprehensive coverage your luxury property demands.

Essential Coverage Options for Luxury Homes

Extended Replacement Cost Protection

Standard replacement cost coverage stops at your policy limit, but construction costs spike significantly after major disasters according to the Insurance Information Institute. Extended replacement cost coverage provides 125-150% above your dwelling limit, which means a $2 million policy extends to $3 million when contractors demand premium prices. We recommend 150% extensions for homes with custom millwork, imported materials, or unique architectural features that require specialized craftsmen. This coverage costs roughly 5-10% more in premiums but prevents devastating gaps when reconstruction costs exceed expectations.

Personal Property Limits That Actually Work

Traditional policies cap personal property at 50% of dwelling coverage with restrictive sub-limits like $2,500 for jewelry or $5,000 for electronics. High value policies offer blanket coverage of $500,000 to $2 million for contents without restrictive categories. Art collections, wine cellars worth $100,000, and custom furniture receive full replacement value without depreciation.

Smart luxury homeowners schedule individual items worth $25,000 or more separately, which provides agreed value coverage and eliminates appraisal disputes during claims. Too many clients discover their $75,000 watch collection only receives $2,500 under standard policies.

Additional Living Expenses Without Time Restrictions

Standard policies limit additional living expenses to 12-24 months, but luxury home reconstruction takes 18-36 months according to the National Association of Home Builders. High value policies provide unlimited time periods and higher expense limits that match your actual lifestyle costs. Renting a comparable luxury property costs $15,000-30,000 monthly in Dallas (plus storage for valuable collections and temporary security services). Loss of use coverage should match 100% of your dwelling limit rather than the typical 30% found in standard policies.

These coverage enhancements come at a cost, and several factors determine exactly how much you’ll pay for comprehensive protection.

Factors That Affect High Value Home Insurance Premiums

Property Value and Construction Materials Drive Base Costs

Property value serves as the foundation for premium calculations, but construction materials create the real cost differences. Homes built with imported marble, hand-carved millwork, or custom metalwork cost significantly more to insure than properties with standard materials. A $2 million home with basic materials might cost $4,000 annually, while the same value home with Venetian plaster walls and Brazilian hardwood floors reaches $6,500. Carriers examine architectural plans and conduct on-site inspections to assess reconstruction complexity. Clients often express shock when their seemingly modest renovations with premium materials double their insurance costs.

Geographic Risk Zones Determine Base Rates

Texas divides into distinct risk zones that dramatically affect premiums. Coastal properties within 15 miles of the Gulf pay hurricane surcharges of $2-4 per $1,000 of coverage according to the Texas Department of Insurance. Hail-prone areas like North Dallas see 25-35% higher rates than protected Hill Country locations. Properties in high-crime ZIP codes (like certain areas of Houston) face 15-20% security surcharges, while gated communities in Southlake receive 10-15% discounts. Wildfire risk areas in West Texas trigger additional premiums, and flood zone designations add separate coverage requirements that standard policies exclude entirely.

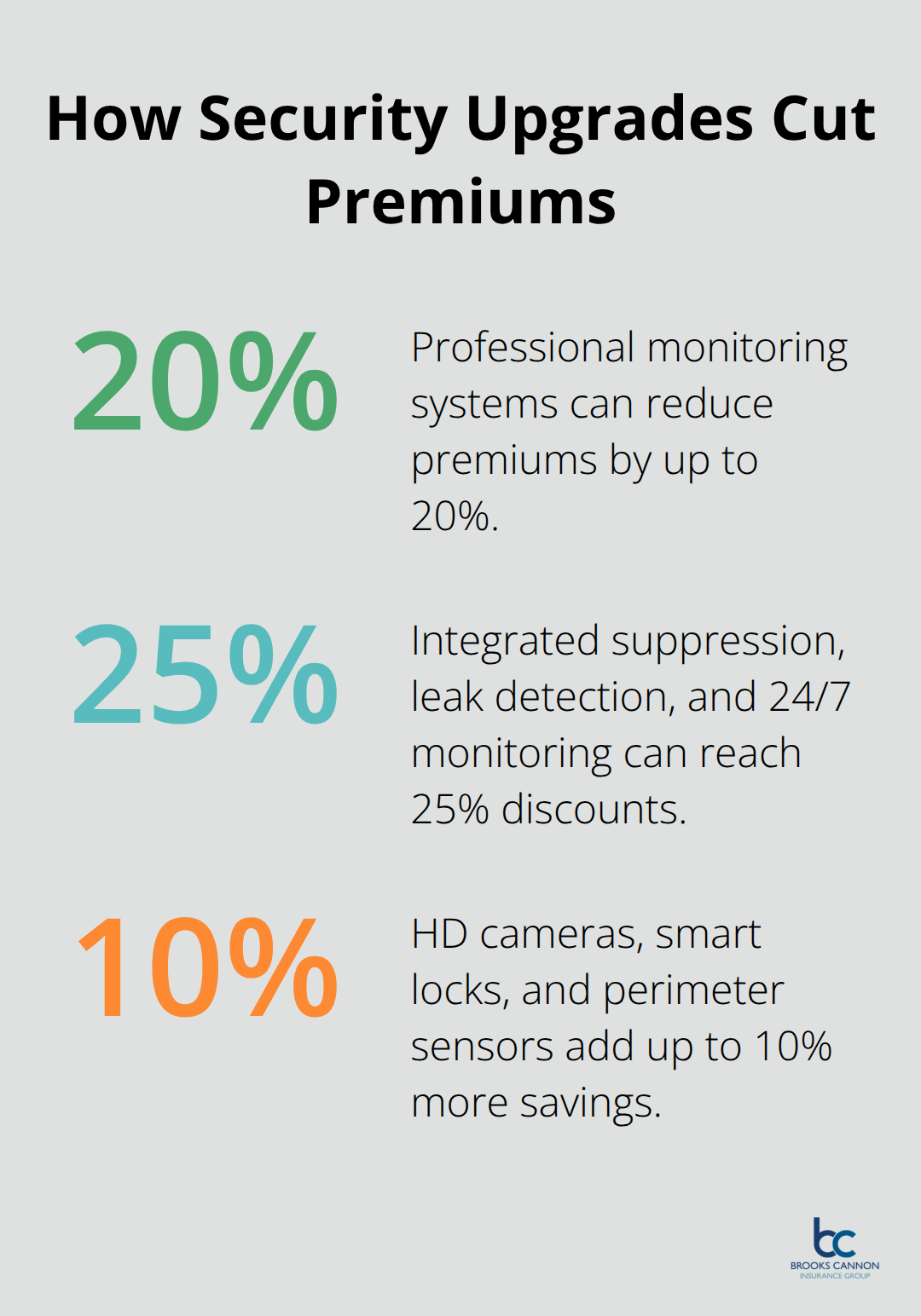

Security Systems Cut Premiums Substantially

Professional monitoring systems reduce premiums by 15-20%, but smart home technology delivers even better savings. Homes with integrated fire suppression systems, leak detection sensors, and 24/7 professional monitoring qualify for maximum discounts that reach 25% according to the Insurance Information Institute. High-definition camera systems with cloud storage, smart locks, and perimeter sensors create additional 5-10% reductions.

Properties with on-site security staff or guard gates receive the highest discounts (sometimes reaching 30% off base premiums). Too many homeowners install basic systems that provide minimal savings instead of comprehensive solutions that maximize protection and discounts.

Final Thoughts

High value home insurance in Texas requires three essential steps to protect your investment properly. You must obtain professional property appraisals that document your home’s true replacement cost and catalog valuable personal property. You need to work with carriers that specialize in luxury properties rather than settle for standard policy upgrades. Annual policy reviews help you adjust coverage as property values change and you acquire new assets.

Independent agents provide access to multiple specialized carriers that standard captive agents cannot offer. We at Brooks Cannon Insurance Group work with top-rated carriers to compare coverage options and pricing for each client’s unique situation. Independent agencies negotiate better terms and advocate for clients during claims rather than represent single insurance companies.

Your luxury property represents years of financial success and personal investment. Standard homeowners policies leave massive coverage gaps that could cost hundreds of thousands during claims (often more than the annual premium difference between adequate and inadequate coverage). High value home insurance Texas policies provide the comprehensive protection your investment demands, from extended replacement costs to unlimited personal property coverage.