Your jewelry collection represents years of careful selection and significant financial investment. Standard homeowners insurance typically caps jewelry coverage at $1,500 to $2,500, leaving expensive pieces dangerously underprotected.

High value jewelry insurance fills this gap with specialized coverage designed for items that deserve better protection. We at Brooks Cannon Insurance Group help Dallas residents secure comprehensive policies that match the true worth of their valuables.

What Qualifies as High Value Jewelry

The line between standard homeowners coverage and specialized jewelry insurance typically falls around $1,500. Pieces valued above this threshold need dedicated protection because homeowners policies simply weren’t designed to handle expensive jewelry claims. Engagement rings, luxury watches, and heirloom pieces commonly exceed this limit, and each one deserves individual attention.

The Foundation: Professional Appraisals

An appraisal establishes the foundation of proper coverage. Professional jewelers document the exact materials, gemstone quality, and current market value of your pieces. Without this documentation, insurance companies have little reason to pay claims at full replacement cost. You should update appraisals every two to three years because jewelry values fluctuate with market conditions and material costs.

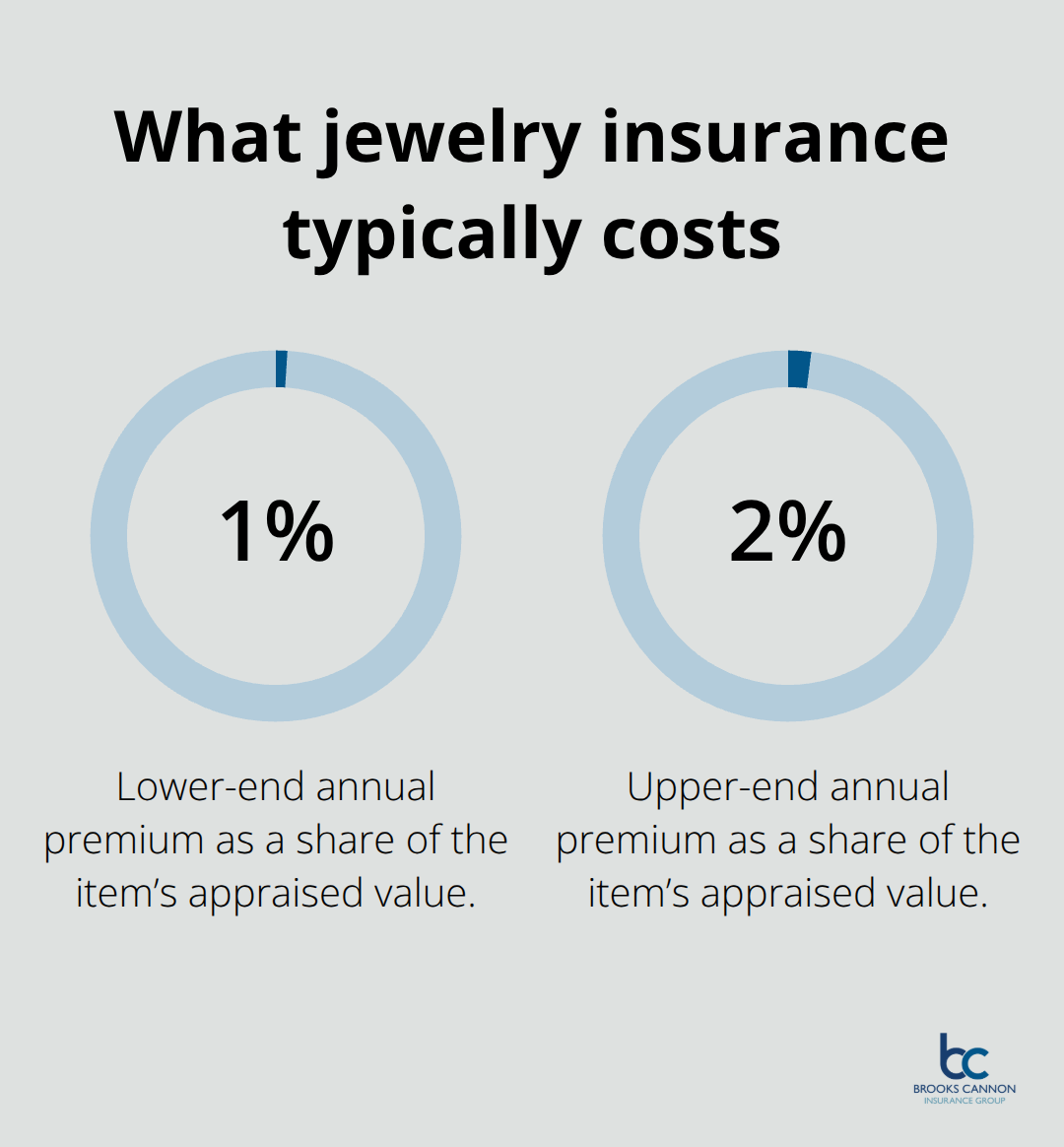

For a $10,000 diamond ring, you might pay roughly $100 to $200 annually for specialized coverage, which breaks down to about 1 to 2 percent of the item’s appraised value. This cost is far cheaper than the risk of losing thousands of dollars if your piece disappears, gets stolen, or suffers accidental damage.

When Your Jewelry Needs Special Protection

High value pieces that travel with you require worldwide coverage that homeowners policies rarely provide. A diamond necklace worn while traveling internationally, an expensive watch worn daily, or a collection stored at home all face different risk profiles. Stolen jewelry claims represent a significant portion of homeowners insurance disputes in Texas, particularly in urban areas like Dallas where theft rates run higher.

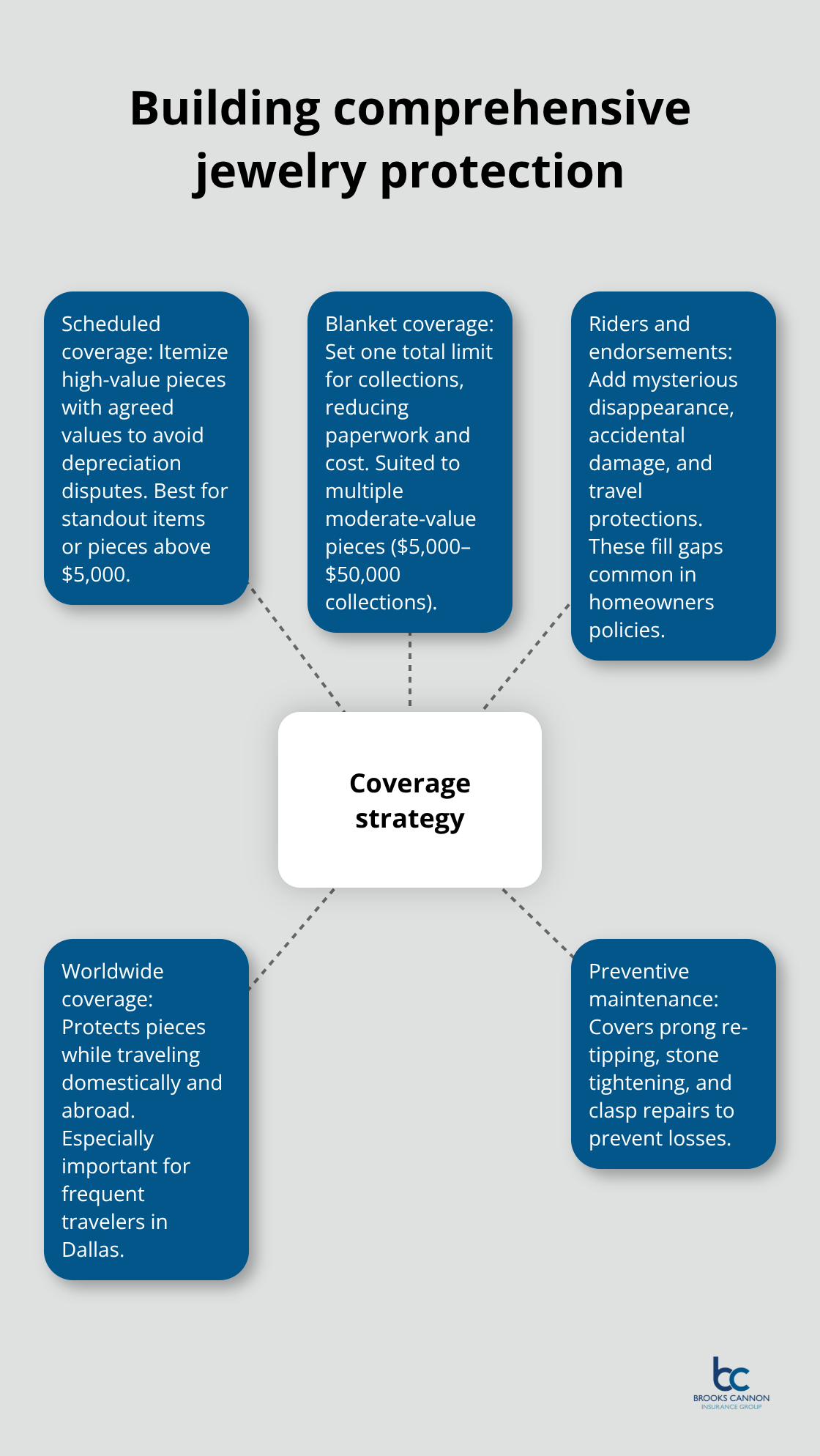

Scheduled personal property coverage itemizes each piece with its own agreed-upon value, which eliminates depreciation arguments when you file a claim. This approach works best for individual pieces valued above $5,000 or collections worth $15,000 or more. For smaller collections between $5,000 and $10,000, blanket coverage provides cost-effective protection without itemizing every single piece. The key distinction matters: scheduled coverage means the insurance company agrees upfront on what your ring or watch is worth, while actual cash value policies subtract depreciation, leaving you with far less money after a loss.

Documentation That Protects Your Investment

A professional appraisal includes detailed photographs, gemstone certifications, metal composition, and current replacement value. You should keep this documentation in a safe location separate from your home, such as a safe deposit box. Photographs alone don’t establish value or condition for insurance purposes.

Some insurers accept certifications from organizations like the Gemological Institute of America, which provide independent verification of diamond and gemstone quality. Receipts from the original purchase help, but market values change constantly, making older receipts unreliable for coverage decisions. For inherited jewelry, a new appraisal proves essential because sentimental value doesn’t appear on insurance documents. The cost of a professional appraisal typically ranges from $75 to $200 (depending on the complexity and value of the piece), money well spent when it determines how much your insurance company will actually pay after a loss.

Understanding what qualifies as high value jewelry and how to document it properly sets the stage for selecting the right coverage options that match your collection’s true worth.

Coverage Options for High Value Jewelry

Scheduled Coverage Protects Your Exact Investment

Scheduled personal property coverage lists each piece individually with a pre-agreed value that both you and the insurance company accept upfront. When you file a claim, the insurer pays that agreed amount without depreciation deductions or arguments about current market value. For a $12,000 engagement ring, scheduled coverage means the insurance company commits to paying $12,000 if the ring is lost, stolen, or damaged beyond repair.

This certainty eliminates the dispute that often occurs with actual cash value policies, where insurers subtract depreciation and reduce your payout significantly. Actual cash value policies calculate what your jewelry is worth today minus wear and tear, potentially leaving you with significantly less than replacement cost. In Dallas, where jewelry theft claims increased substantially over the past five years, scheduled coverage protects you from the depreciation trap that catches most homeowners off guard.

Cost and Affordability of Scheduled Protection

The cost difference between coverage types matters significantly. Scheduled coverage typically runs 1 to 2 percent of the item’s appraised value annually, so a $10,000 piece costs roughly $100 to $200 per year. This small premium provides certainty that your investment receives full replacement value when you need it most.

Blanket Coverage for Multiple Pieces

Blanket jewelry coverage offers a different path for collectors who own multiple pieces valued between $5,000 and $50,000. Instead of scheduling each item separately, blanket coverage provides one total limit for your entire jewelry collection, reducing paperwork and administrative overhead that lowers your premium. This approach works well when you own several pieces in the moderate range rather than a few extremely high value items.

Strategic Riders That Complete Your Protection

Additional riders and endorsements layer on specific protections like worldwide coverage for travel, mysterious disappearance claims when jewelry vanishes without explanation, and accidental damage protection that covers everyday mishaps like losing a stone from a setting. Many policies exclude mysterious disappearance by default, making this rider essential if you want coverage when you simply cannot locate a piece.

Preventive maintenance coverage through specialized jewelry policies covers prong re-tipping, stone tightening, and clasp replacement before damage occurs, extending the life of your collection. Dallas residents who travel frequently should prioritize worldwide coverage since standard homeowners policies provide zero protection outside your home state. The combination of blanket coverage with strategic riders creates comprehensive protection without the cost of scheduling every single piece, making it the practical choice for most collections.

Understanding these coverage options positions you to evaluate why standard homeowners insurance leaves your jewelry dangerously exposed.

Why Your Homeowners Policy Leaves Jewelry Unprotected

The Hard Coverage Limits That Leave You Exposed

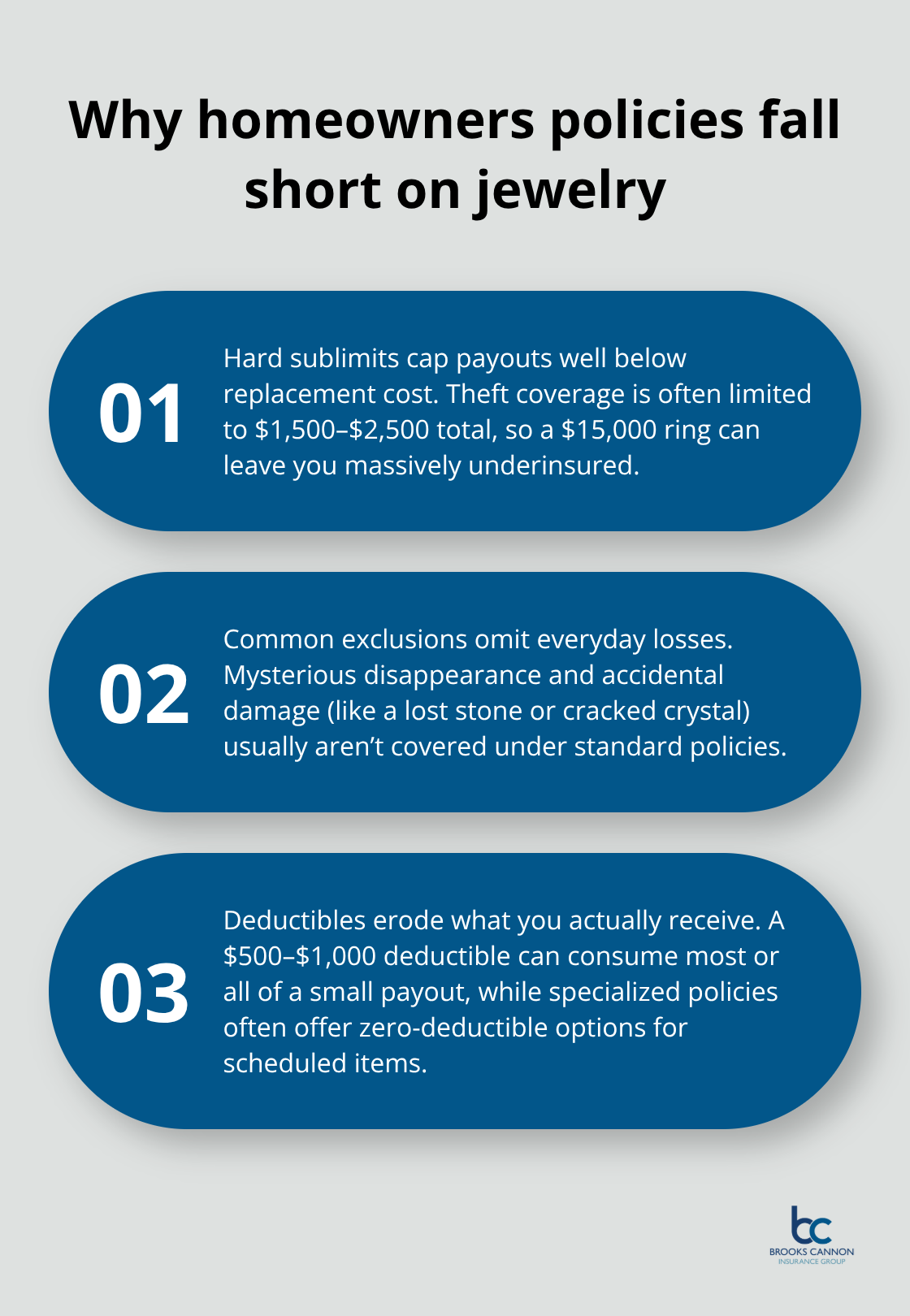

Your homeowners insurance policy contains a hard cap on jewelry coverage that most Dallas residents never notice until they file a claim. Standard homeowners policies limit jewelry theft coverage to between $1,500 and $2,500 total, regardless of how many pieces you own or what they actually cost to replace.

Texas homeowners policies like the HO-B form set jewelry theft sub-limits at $500, while newer policies such as Nationwide’s HO-542 increase this only to $1,000. A $15,000 engagement ring receives protection for just $1,000, leaving you personally responsible for the remaining $14,000 in losses.

The gap between what your policy covers and what your jewelry costs creates genuine financial exposure that catches homeowners off guard when theft or damage occurs. Dallas experiences higher jewelry theft rates than many Texas cities due to urban density and property crime patterns, making this coverage gap particularly dangerous for residents in our area. Even if you own multiple pieces, homeowners policies lump all jewelry together under one low limit rather than protecting each item individually.

Exclusions That Standard Policies Won’t Cover

Homeowners policies exclude many common jewelry loss scenarios that specialized coverage handles. Mysterious disappearance-when you simply cannot locate a piece-receives zero protection under standard homeowners insurance, yet this represents a significant portion of jewelry claims. Accidental damage like losing a stone from a ring setting or cracking a watch crystal falls outside most homeowners coverage because these policies focus on sudden, catastrophic losses rather than everyday mishaps.

The Deductible Trap That Reduces Your Payout

Your homeowners deductible also applies to jewelry claims, meaning you pay $500, $1,000, or more out of pocket before the insurance company contributes anything, further reducing your effective coverage. If your ring is worth $12,000 and your policy covers only $1,500 with a $1,000 deductible, you receive just $500 from insurance while absorbing $11,500 in personal losses.

Specialized jewelry insurance eliminates this deductible trap through zero-deductible options for scheduled items and agreed values that reflect actual replacement costs rather than depreciated amounts. The combination of low limits, broad exclusions, and high deductibles transforms standard homeowners coverage into inadequate protection for anything beyond costume jewelry or inexpensive pieces.

Final Thoughts

Your jewelry collection deserves protection that matches its actual value, not the inadequate limits buried in your homeowners policy. High value jewelry insurance provides the certainty that your pieces receive full replacement cost when loss, theft, or damage occurs. The difference between standard homeowners coverage and specialized jewelry protection often means the difference between recovering your investment and absorbing thousands of dollars in personal losses.

Start by gathering your jewelry and obtaining professional appraisals for pieces valued above $1,500. These appraisals establish the foundation for accurate coverage decisions and accelerate claims processing if you ever need to file. Once you have documentation in place, you can select between scheduled coverage for individual high-value pieces or blanket coverage for collections, depending on what makes sense for your situation.

We at Brooks Cannon Insurance Group work with Dallas residents to build jewelry protection plans that actually cover what your pieces are worth. Our licensed experts understand the unique risks that Dallas homeowners face and can guide you through the process of evaluating your current coverage, identifying gaps, and selecting the right high value jewelry insurance options. Contact us today to discuss how we can help secure your valuables.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation