Building a home or commercial property in the Dallas area requires protecting your investment from the ground up. Builders risk insurance price varies significantly based on your project’s scope, location, and construction methods.

We at Brooks Cannon Insurance Group help contractors and property owners understand what drives these costs so you can budget accurately. This guide breaks down the real factors affecting your premiums and shows you concrete ways to reduce them.

What Really Drives Your Builders Risk Premium

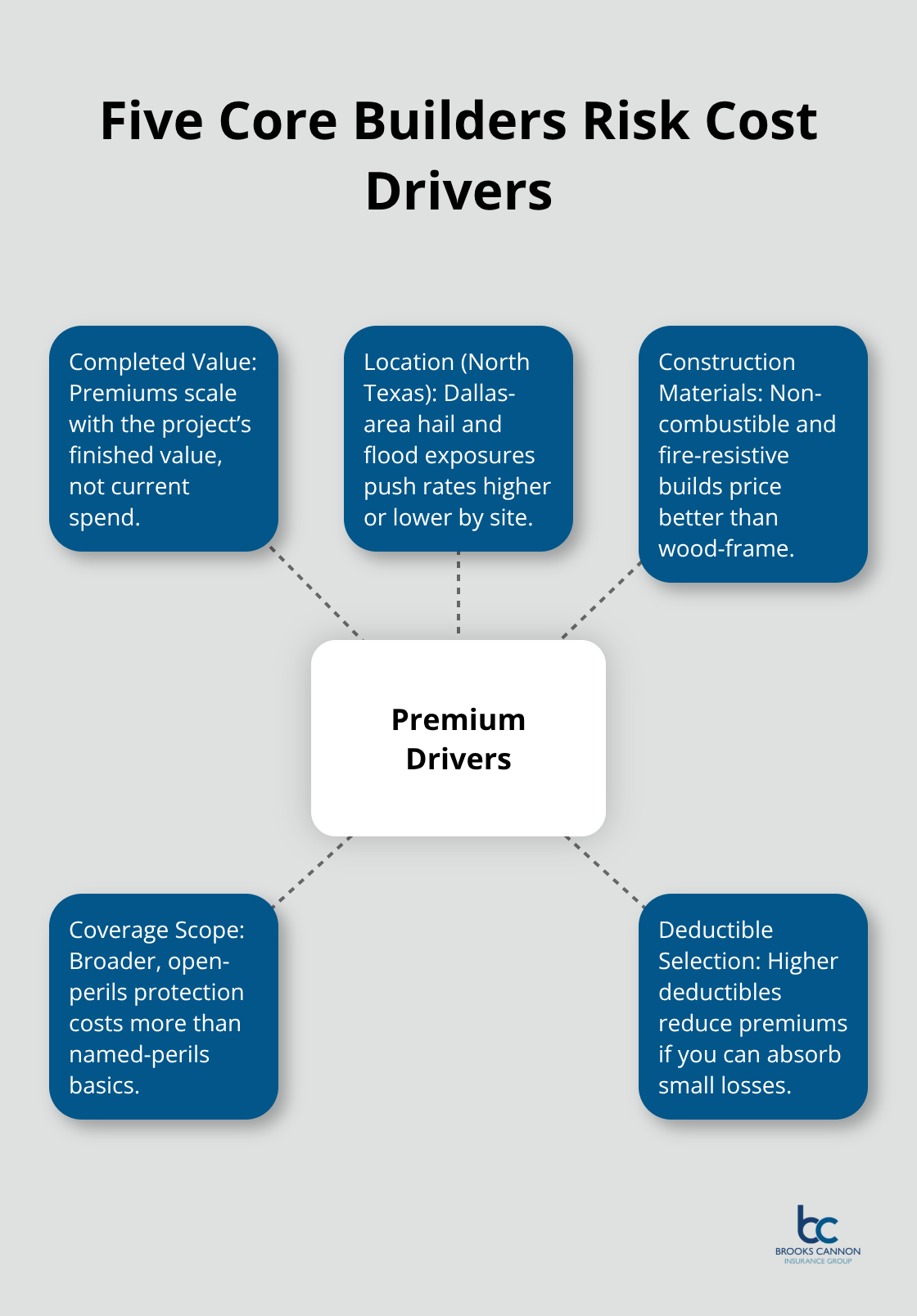

Project size matters, but not in the way most people think. A $500,000 renovation doesn’t simply cost twice as much to insure as a $250,000 one. Insurers price based on completed value, construction type, and duration instead. A $250,000 project typically costs $2,500 to $10,000 annually, while a $500,000 project ranges from $5,000 to $20,000. The variance comes from how your project is built, where it sits, and what materials you choose.

Location Drives Your Biggest Cost

In Dallas, location is your single biggest cost driver. Projects in high-risk flood zones or areas prone to hail damage cost substantially more than those in lower-risk neighborhoods. North Texas sits directly in Hail Alley, where billion-dollar hail events have caused over $500 million in construction-related damages in single storms. Your proximity to fire stations, flood zones, and weather exposure all factor into your final quote.

Construction Type Changes Everything

Wood-frame buildings cost significantly more to insure than steel or concrete structures. Fire-resistive masonry and non-combustible construction can reduce your premium by 15% to 25% compared to wood-frame equivalents. The NFPA reports that construction fires cause approximately $370 million in direct damages annually, which is why insurers charge more for flammable materials. Steel and concrete structures present lower fire risk, so carriers reward you with better rates.

Safety Records and Deductibles Lower Your Costs

Your contractor’s experience and safety record influence pricing, though less dramatically than construction type or location. Contractors with documented loss histories pay higher premiums, while those with clean safety records receive better terms. If your team implements strong site security, maintains equipment properly, and follows safety protocols, some carriers offer modest discounts.

Deductibles range from $500 to $5,000, and you can lower your premium directly by selecting a higher deductible. A $5,000 deductible might save you 10% to 20% compared to a $500 option, making it worth considering if your project has adequate cash reserves. Understanding these cost drivers helps you make informed decisions about where to invest in coverage and where you can afford to take on more risk yourself.

What You’ll Actually Pay for Builders Risk

Your premium depends on whether you’re building a $250,000 residential renovation or a $3,000,000 commercial project, and the numbers vary considerably within each category. For residential renovations in the Dallas area, expect to pay around $4,000 annually on a $200,000 project, which breaks down to roughly 2% of your total construction value. A $500,000 custom home typically costs between $5,000 and $20,000 per year, depending on whether you choose basic named-perils coverage or broader open-perils protection. Commercial projects follow similar percentage ranges but with higher absolute costs-a $3,000,000 commercial build runs approximately $6,480 annually, though Dallas projects often cost less due to lower coastal risk. The key insight is that premiums scale with your project’s completed value, not what you’ve spent so far, so a half-finished $1,000,000 project still costs more to insure than a fully completed $250,000 one. Installation work represents the lowest-cost category since these projects finish quickly and carry minimal exposure, while remodeling projects on existing structures typically cost 15% to 30% more than new construction because insurers account for hidden structural risks and the complexity of working around existing conditions.

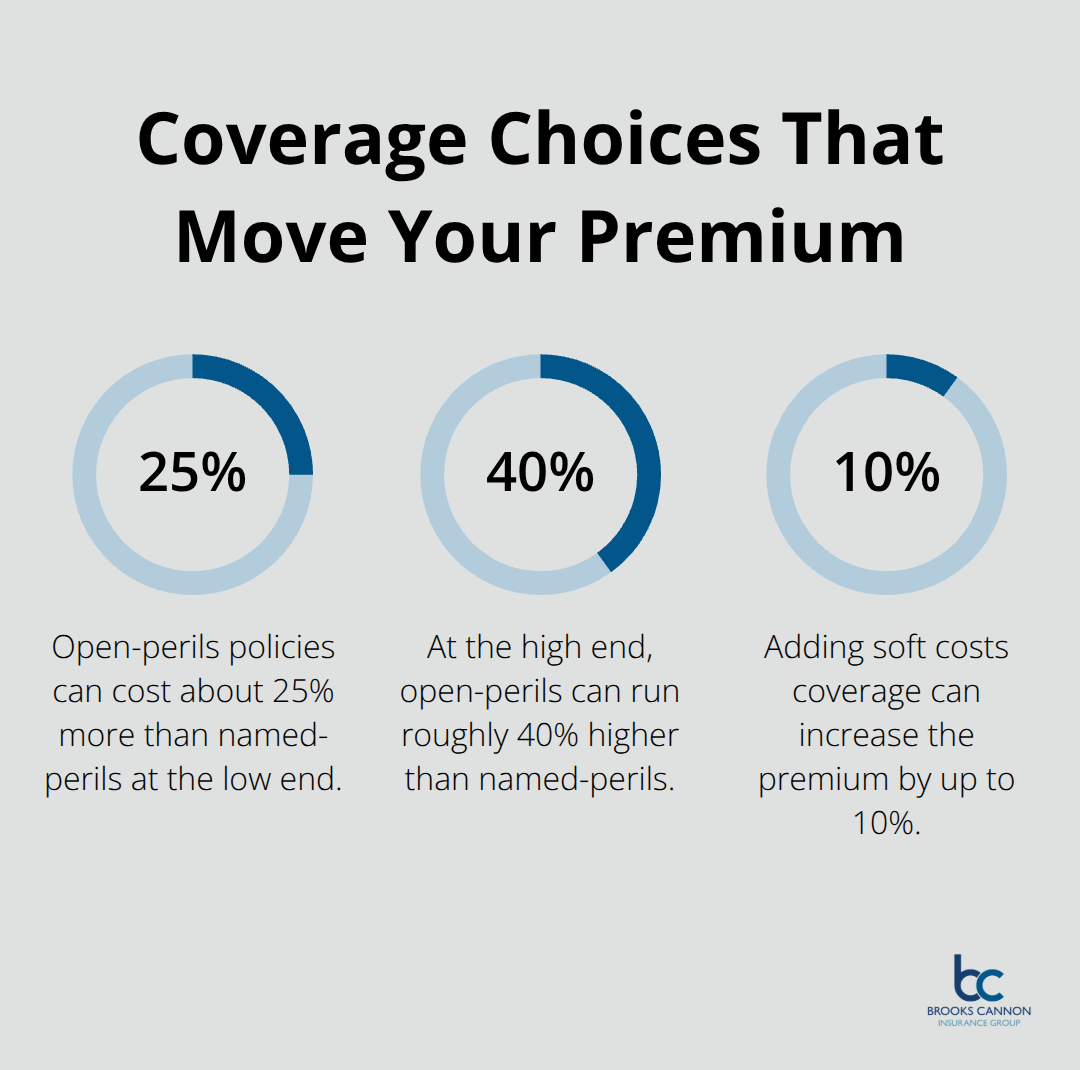

Coverage scope determines your final bill

Open-perils policies cost substantially more than named-perils options, sometimes 25% to 40% higher, because they protect against nearly every peril except those specifically excluded rather than only covering listed dangers. Named-perils coverage protects against fire, wind, hail, theft, and vandalism but excludes water damage, equipment breakdown, and other risks unless you add endorsements. Most Dallas contractors choose named-perils as their base and add specific endorsements for flood or earthquake coverage, which is the practical approach since you only pay for protections your project actually needs. Soft costs coverage-which reimburses extended loan interest, lease administration, and extra labor costs from project delays-adds roughly 5% to 10% to your annual premium but proves invaluable if your project extends beyond schedule.

How deductibles affect your bottom line

Your deductible choice directly impacts your monthly or annual payment. A $5,000 deductible instead of $500 typically saves 10% to 20% on your premium, making it worth the trade-off if you have adequate reserves to cover smaller losses yourself. This decision matters most for contractors who manage multiple projects and can absorb occasional out-of-pocket expenses without disrupting cash flow. Lower deductibles provide peace of mind but cost noticeably more, so align your choice with your project’s financial cushion and your risk tolerance.

How to Actually Cut Your Builders Risk Costs

Bundle Coverage to Unlock Real Savings

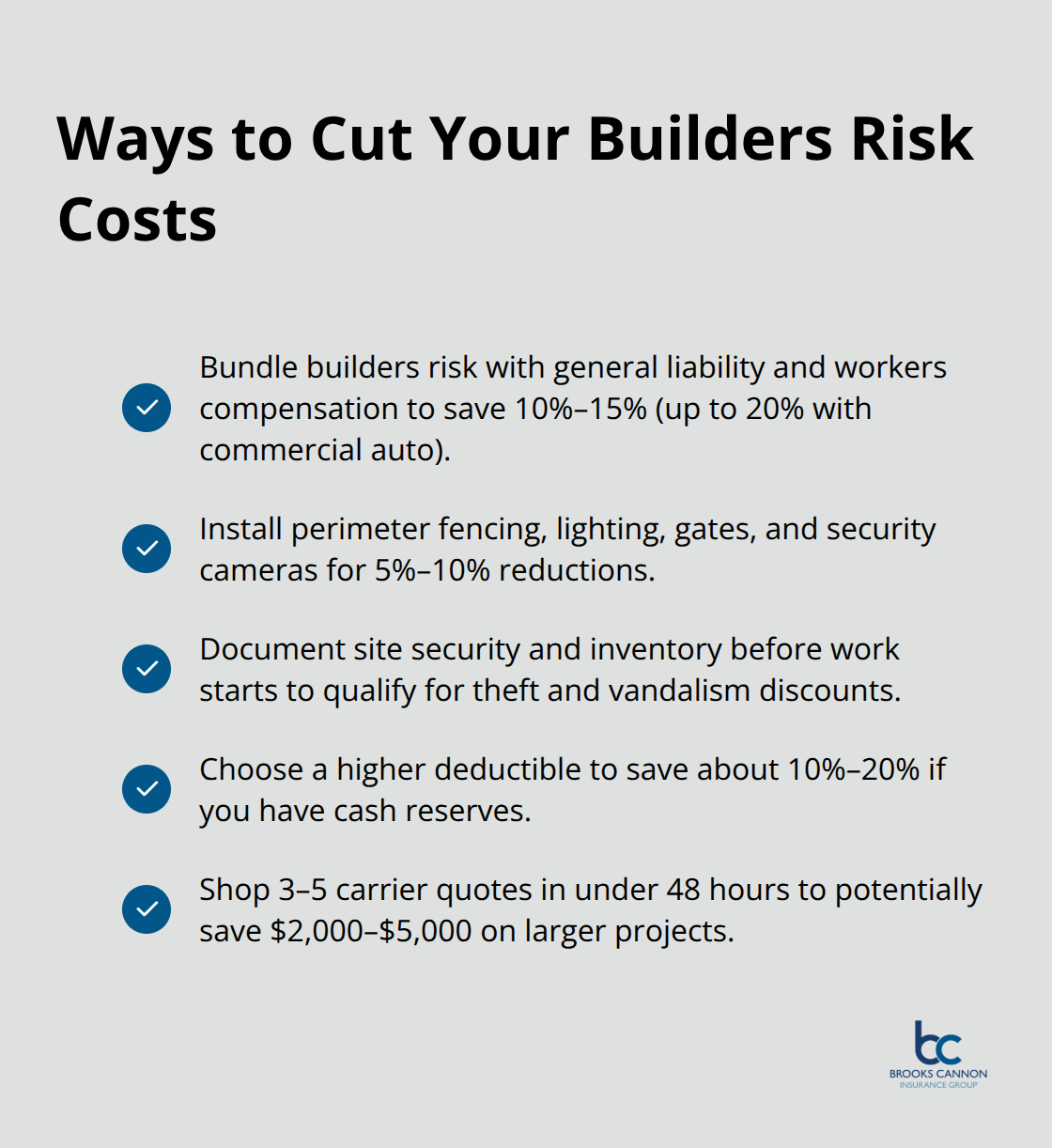

Combining builders risk with general liability and workers compensation coverage produces savings that most contractors overlook. Carriers typically offer 10% to 15% discounts when you consolidate multiple policies under one program, and some programs extend that to 20% if you add commercial auto coverage. The math works in your favor: a contractor paying $8,000 for builders risk, $3,000 for general liability, and $5,000 for workers comp saves roughly $3,200 annually through bundling rather than shopping each policy separately. This advantage matters even more in Dallas where carrier competition remains fierce. The key is confirming your bundled program covers all project phases, from groundbreaking through occupancy, without gaps between policy periods.

Invest in Site Security for Premium Reductions

Site security directly impacts your premium, and carriers reward documented loss prevention with tangible discounts. Installing perimeter fencing, locking gates, motion-activated lighting, and security cameras can reduce your premium by 5% to 10% because theft and vandalism represent major claim drivers. Documentation proves essential here-photograph your security measures and maintain inventory records before work starts, as insurers require proof that protections were in place before approving theft claims. Contractors who maintain clean, organized job sites with equipment stored securely and materials accounted for also negotiate better rates.

Shop Multiple Quotes to Find Your Best Rate

Shopping multiple quotes reveals dramatic pricing differences that justify the effort. Obtaining formal quotes from three to five carriers typically takes less than 48 hours and can save $2,000 to $5,000 annually on projects valued above $500,000. Each carrier weighs location, construction type, and your safety history differently, so what costs $12,000 with one insurer might run $9,500 with another. An independent agent who shops your project details across numerous carriers provides the most comprehensive comparison, capturing available discounts and finding carriers willing to write your specific risk profile.

Final Thoughts

Builders risk insurance price depends on five core factors: your project’s completed value, location within North Texas, construction materials, coverage scope, and deductible selection. A $250,000 residential project costs roughly $2,500 to $10,000 annually, while a $500,000 custom home runs $5,000 to $20,000 per year. The percentage typically falls between 1% and 4% of your total construction value, though Dallas projects often land on the lower end due to reduced coastal exposure compared to other Texas regions.

Your next step involves requesting three to five formal quotes from different carriers, a process that takes less than 48 hours and frequently saves thousands of dollars because each insurer prices your specific risk differently. When you request quotes, provide your project’s completed value, construction type, location, timeline, and any existing safety measures you’ve implemented. Higher deductibles and bundled coverage with general liability and workers compensation both reduce your final cost meaningfully, so discuss these options with each carrier.

We at Brooks Cannon Insurance Group work with multiple top-rated insurance carriers to find the best builders risk coverage and pricing for your Dallas-area project. Our licensed team understands North Texas construction risks, from Hail Alley exposure to local flood zones, and we shop your project details across numerous carriers to capture available discounts. Contact Brooks Cannon Insurance Group today to get an accurate quote and protect your construction investment from groundbreaking through occupancy.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation