Landlord insurance protects your investment, but understanding what drives your landlord insurance cost is the first step toward smart financial planning. Property value, location, tenant quality, and security features all play a role in determining your premium.

We at Brooks Cannon Insurance Group help Dallas-area landlords navigate these factors and find coverage that fits their budget. The right strategy can significantly reduce what you pay while keeping your rental property fully protected.

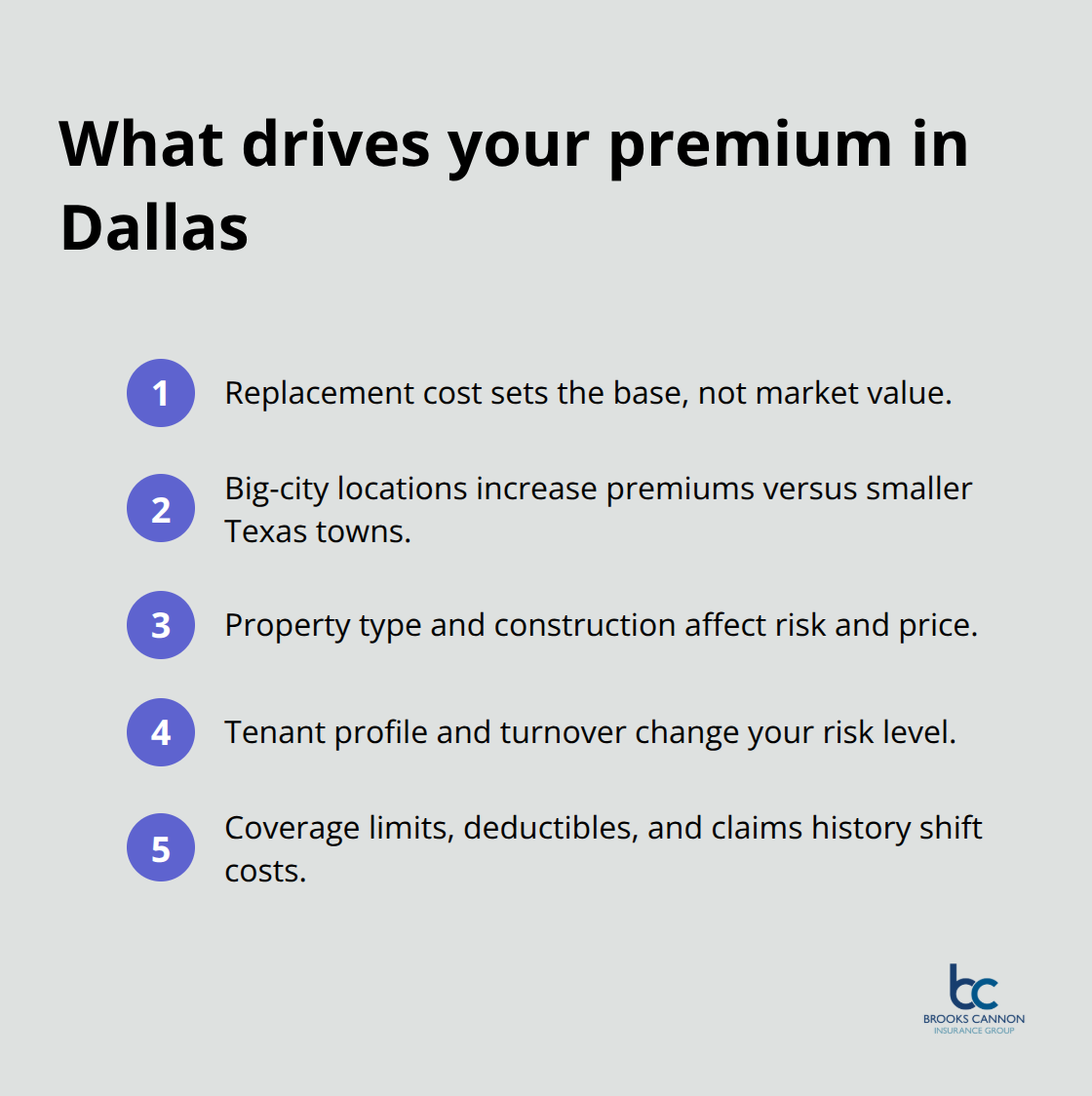

What Really Drives Your Landlord Insurance Premium

Your landlord insurance premium reflects hard numbers that insurers calculate with precision. The replacement cost of your property-not its market value-forms the foundation. If your Dallas rental home would cost $250,000 to rebuild from the ground up, insurers use that figure, not the $280,000 you might sell it for. Location intensifies costs across the Dallas area. Properties in Dallas, Houston, and San Antonio carry higher premiums because rebuilding costs and rental values significantly exceed those in smaller Texas towns. A single-family rental in Dallas typically costs between $1,300 and $1,900 annually, roughly 15 to 25 percent more than standard homeowners insurance according to Insurance Information Institute data. Multi-family properties valued near $600,000 can reach $2,000 to $4,000 or higher per year.

How Property Age and Condition Shape Your Rate

Your property’s age and condition directly impact your rate. A well-maintained 10-year-old home with updated electrical and plumbing systems costs less to insure than a 40-year-old property with deferred maintenance. Materials matter significantly-brick construction typically costs less to insure than wood frame because it presents lower fire risk. Insurers reward property owners who maintain their buildings consistently. Regular upkeep reduces the likelihood of claims and signals responsible ownership to underwriters.

Property Type and Structure Determine Base Cost

A single-family rental, duplex, triplex, or apartment building each carries different risk profiles. Single-family rentals represent the cheapest option to insure because they present straightforward risk. Duplexes and triplexes increase complexity and exposure. Apartment buildings with four or more units shift into commercial territory and cost substantially more. The structure type matters as much as the unit count. Older wood-frame buildings cost more than newer concrete or steel structures.

Tenant Profile Creates Measurable Risk Differences

Your tenant profile shapes your premium significantly. Long-term tenants with stable income reduce your premium compared to short-term rentals. If you rent to short-term tenants through platforms like Airbnb, you pay substantially more or require specialized endorsements. Insurers view frequent tenant turnover as higher risk for property damage and vacancy periods. Tenant screening practices matter too-insurers recognize that careful background and credit checks reduce claims frequency.

Claims History and Coverage Choices Control Your Cost

Claims history affects your rate at renewal. A single claim can raise your premium by 5 to 15 percent depending on severity. Multiple claims within a few years make you a higher-risk client and can limit which insurers will cover you. Your deductible choice directly controls your premium. A $500 deductible costs more than a $1,000 deductible. A $2,500 deductible costs substantially less but means you absorb more out-of-pocket after a loss. The coverage limits you select matter equally. Requesting $1 million in liability protection costs more than $300,000. Higher dwelling limits and broader coverage like loss of rent protection increase your annual cost but protect your income stream if tenants cannot occupy the property.

Understanding these five factors positions you to make informed decisions about your coverage. The next step involves gathering the specific information insurers need to quote your property accurately.

Getting Quotes That Actually Reflect Your Property

Collect the Details Insurers Need

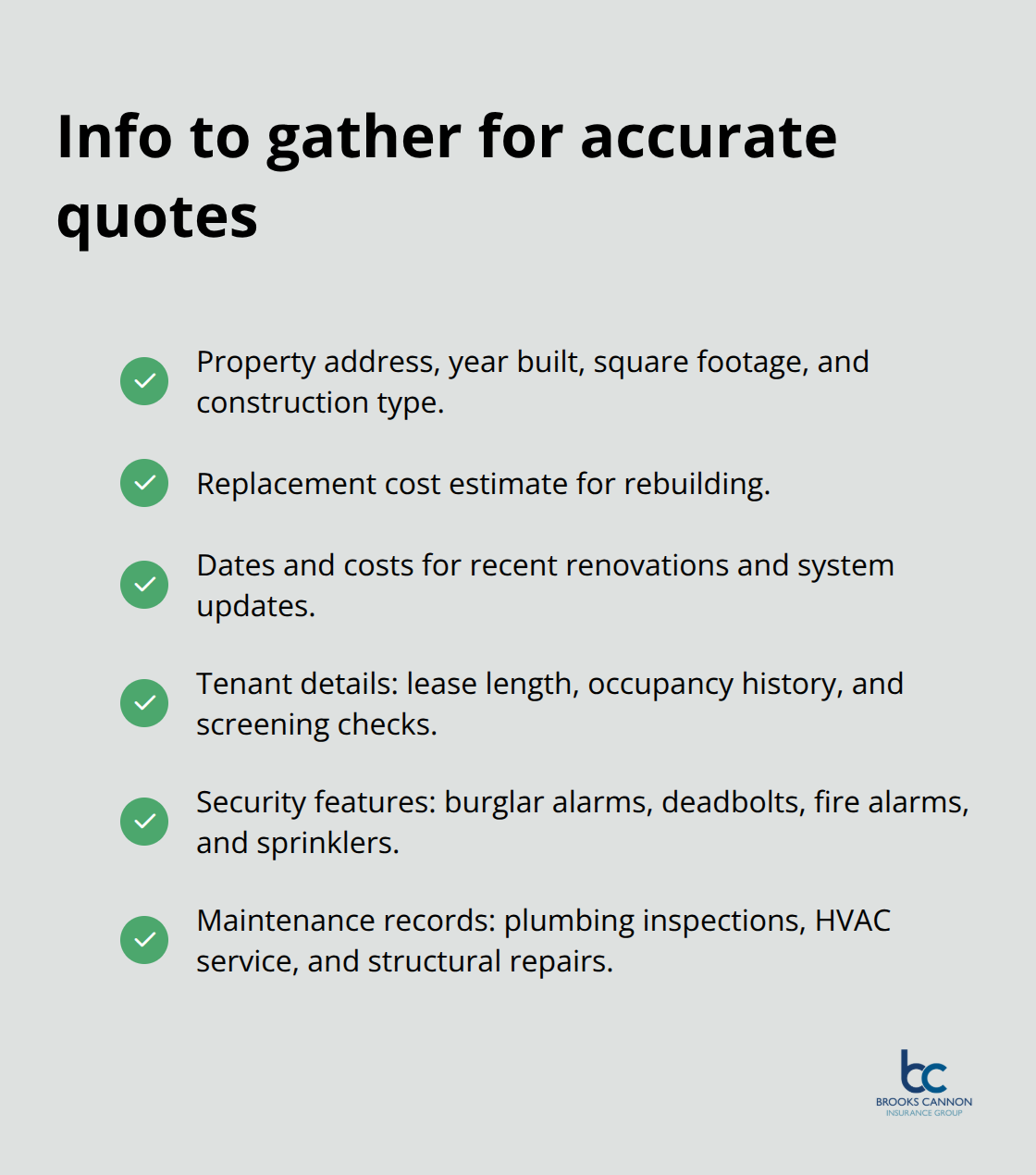

Insurers require specific information about your Dallas rental property to calculate accurate premiums. Start with your property address, year built, square footage, and construction type-wood frame, brick, or concrete. Document the replacement cost estimate for rebuilding; this is not your purchase price or current market value but what it would cost to reconstruct the structure from the ground up. If you renovated your kitchen, updated electrical systems, or replaced the roof within the last five years, have those dates and costs ready. Insurers reward recent improvements because they reduce risk.

Collect information about your tenants as well: lease length, occupancy history, and whether you conduct background and credit checks. Include details about security features-burglar alarms, deadbolts, fire alarms, and sprinkler systems all lower your premium. Property maintenance records matter too; document recent plumbing inspections, HVAC servicing, or structural repairs.

This documentation proves you maintain the property responsibly.

Request Quotes from Multiple Carriers

You should request quotes from at least three to five different insurers rather than stopping at the first offer. Independent agents represent multiple carriers and can pull quotes efficiently without you contacting each company separately. When you compare quotes, focus on identical coverage limits across all proposals. A $250,000 dwelling limit with a $1,000 deductible should appear the same on every quote so you compare actual rates, not coverage differences.

Pay attention to what each policy covers-some include loss of rent protection automatically while others require an endorsement. Verify liability limits match across quotes; most landlords need $1 million in liability coverage for single-family to four-unit properties. Ask each insurer about available discounts: claims-free discounts typically range from 5 to 15 percent, bundling multiple policies saves roughly 15 to 20 percent, and safety feature discounts reward property improvements.

Compare Rates and Identify Real Savings

Monthly cost varies significantly by insurer. One carrier might quote $110 per month while another quotes $160 for the same coverage on an identical property. That $600 annual difference justifies shopping around. When you evaluate proposals, look beyond the headline premium and examine what each carrier actually covers. Some insurers include specific endorsements at no extra charge while others charge separately for the same protection.

The Texas Department of Insurance maintains a searchable database of licensed agents if you want to verify credentials before working with anyone. This step protects you from unlicensed operators and confirms that agents meet state requirements. As an independent agency based in Dallas, we at Brooks Cannon Insurance Group work with multiple top-rated carriers to find the best coverage and pricing for your rental property. Your next step involves understanding how coverage choices and deductible decisions directly impact what you pay each month.

Cut Your Landlord Insurance Premium Without Cutting Coverage

Lower Your Deductible to Save Immediately

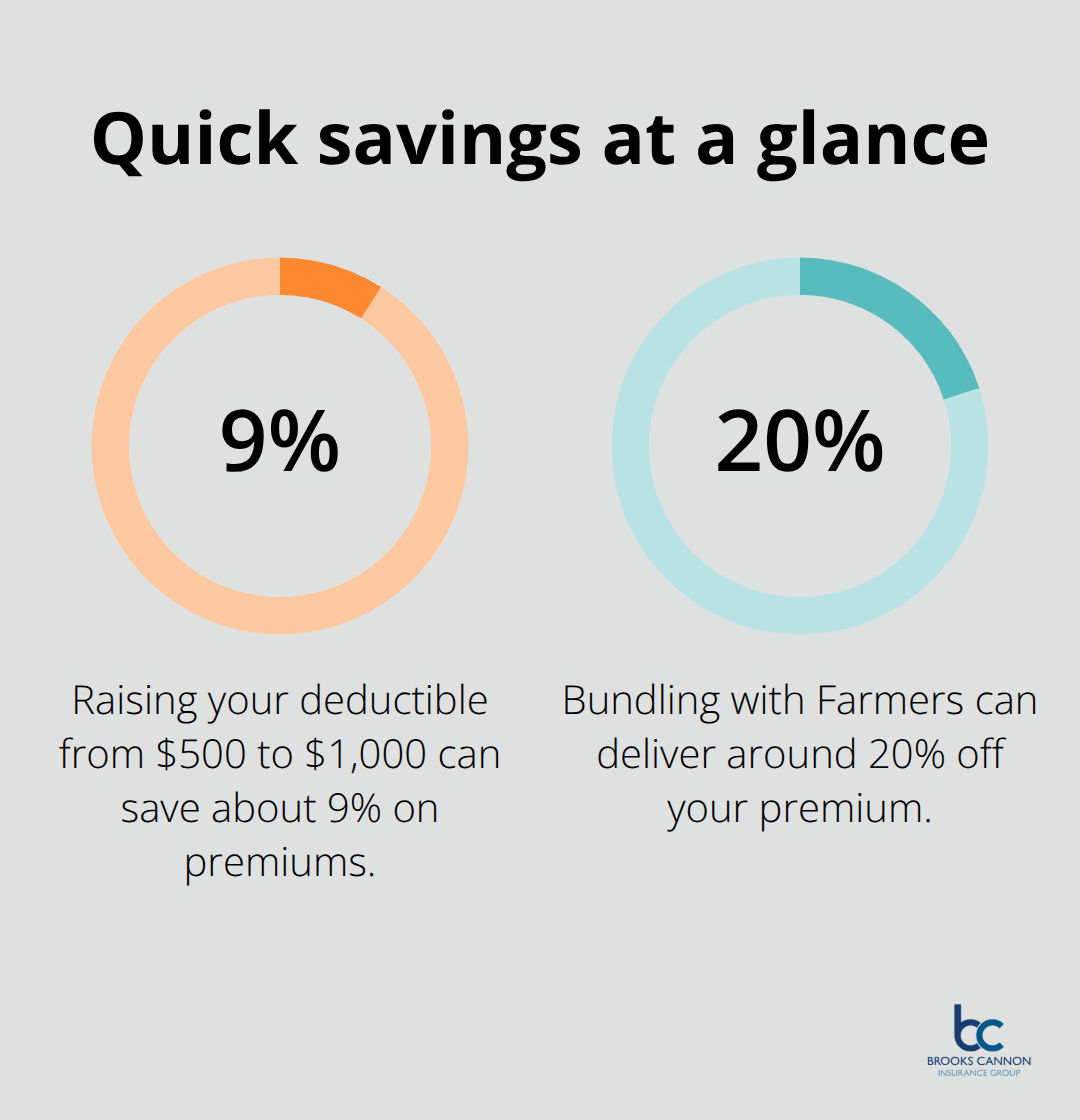

Your deductible is the fastest lever to pull when reducing your landlord insurance premium. Raising your deductible from $500 to $1,000 can save you an average of nearly 9% on your premiums. The math is straightforward: you absorb more out-of-pocket after a claim, but you pay substantially less upfront. This strategy works if you have cash reserves to cover the higher deductible when needed. If you cannot comfortably pay $1,000 after a loss, do not choose that deductible.

Combine Policies to Unlock Multi-Policy Discounts

Bundling multiple policies with one insurer consistently delivers the strongest discounts. Combining your landlord policy with homeowners, auto, or umbrella coverage typically saves 15 to 20 percent on your total premium according to industry data. Some carriers reward bundling even more aggressively. Farmers offers bundling discounts around 20 percent and includes extras like workers compensation and loss control services. Allstate provides Airbnb-specific coverage through HostAdvantage if you rent short-term, which addresses a gap many standard policies leave uncovered.

Consolidating policies simplifies renewals and billing while increasing your negotiating position with carriers.

Invest in Property Security and Maintenance

Property security investments directly reduce your premium because they reduce insurer risk. Installing burglar alarms, deadbolts, fire alarms, and sprinkler systems can lower your premium by 5 to 15 percent depending on the system and carrier. Newer properties with recent electrical and plumbing updates qualify for better rates than older buildings with deferred maintenance. Document these improvements with photos and receipts so you can reference them when requesting quotes. Regular plumbing and electrical inspections catch problems before they become expensive claims.

Screen Tenants Carefully to Reduce Risk

Tenant screening deserves equal weight in your cost management strategy. Long-term tenants with stable income and clean backgrounds reduce your premium compared to short-term rentals. Frequent turnover increases damage risk and vacancy periods, which insurers penalize with higher rates. Conducting thorough background checks and credit verification before approving tenants demonstrates responsible ownership to underwriters and qualifies you for lower premiums at renewal.

Protect Your Claims History

Claims history directly impacts your next renewal rate. A single claim can raise your premium by 5 to 15 percent, so avoiding unnecessary claims matters financially. This means addressing maintenance issues proactively rather than letting them escalate into insurable losses. The combination of these strategies works together. A Dallas landlord who raises their deductible, bundles with auto insurance, installs a security system, and maintains meticulous tenant screening can reduce their annual cost while maintaining solid protection. Shopping quotes annually ensures you capture new discounts and carrier options that emerge each renewal period.

Final Thoughts

Calculating your landlord insurance cost requires you to understand five core factors: replacement cost, location, property type, tenant profile, and your coverage choices. Dallas-area landlords typically pay between $1,300 and $1,900 annually for single-family rentals, roughly 15 to 25 percent more than standard homeowners insurance. Multi-family properties reach $2,000 to $4,000 or higher depending on value and location, and these numbers reflect real risk assessment by insurers rather than arbitrary pricing.

The strategies that reduce your premium work together effectively. Raising your deductible from $500 to $1,000 saves nearly 9 percent immediately, while bundling landlord insurance with auto or homeowners coverage delivers 15 to 20 percent savings. Installing security systems, maintaining your property consistently, screening tenants carefully, and maintaining long-term leases all lower rates by 5 to 15 percent because they reduce the turnover risk that insurers penalize.

Your next step involves you gathering your property details and requesting quotes from multiple carriers rather than settling for the first offer you receive. Comparing proposals from three to five insurers reveals significant price differences for identical coverage, and an independent agent can pull multiple quotes efficiently without requiring you to contact each company separately. We at Brooks Cannon Insurance Group work with multiple top-rated carriers to find the best landlord insurance coverage and pricing for your Dallas rental property, so contact us to discuss your rental property and receive quotes that reflect your actual situation.