If you’re a business owner in Dallas, you’ve likely heard that you need a certificate of commercial general liability insurance. But what exactly is it, and why does your business need one?

We at Brooks Cannon Insurance Group help business owners navigate this requirement every day. Getting your certificate in place protects your business and satisfies the demands of clients, landlords, and partners who need proof of your coverage.

What a Certificate of Commercial General Liability Insurance Actually Is

A certificate of commercial general liability insurance is a one-page document that proves you have active general liability coverage. It’s not your actual insurance policy-it’s a summary that shows the essential details: your insurer’s name, your policy number, coverage limits, effective dates, and the types of protection you carry. When a client, landlord, or contractor asks for proof that you’re insured, this certificate is what they want to see. The Texas Department of Insurance maintains a registry of certificates, and the standard form used across the industry is called ACORD 25, which most insurers issue at no cost to policyholders. You can typically obtain one within hours or a day by contacting your insurer or requesting it online through your policy dashboard.

Why Clients and Partners Demand This Document

Clients, landlords, and subcontractors require certificates because they need assurance that your insurance will cover damages or injuries that might occur during your work relationship. If someone gets injured on a job site or your work causes property damage, your general liability policy protects against third-party claims related to bodily injury and property damage. Without proof that you carry this coverage, many Dallas businesses won’t hire you, lease space to you, or work with you as a contractor. The certificate shows them exactly what your limits are, and having it ready eliminates delays in contracts, bids, and leases; many Dallas projects require certificates within 24 hours to meet bid deadlines, so waiting until the last moment creates unnecessary risk.

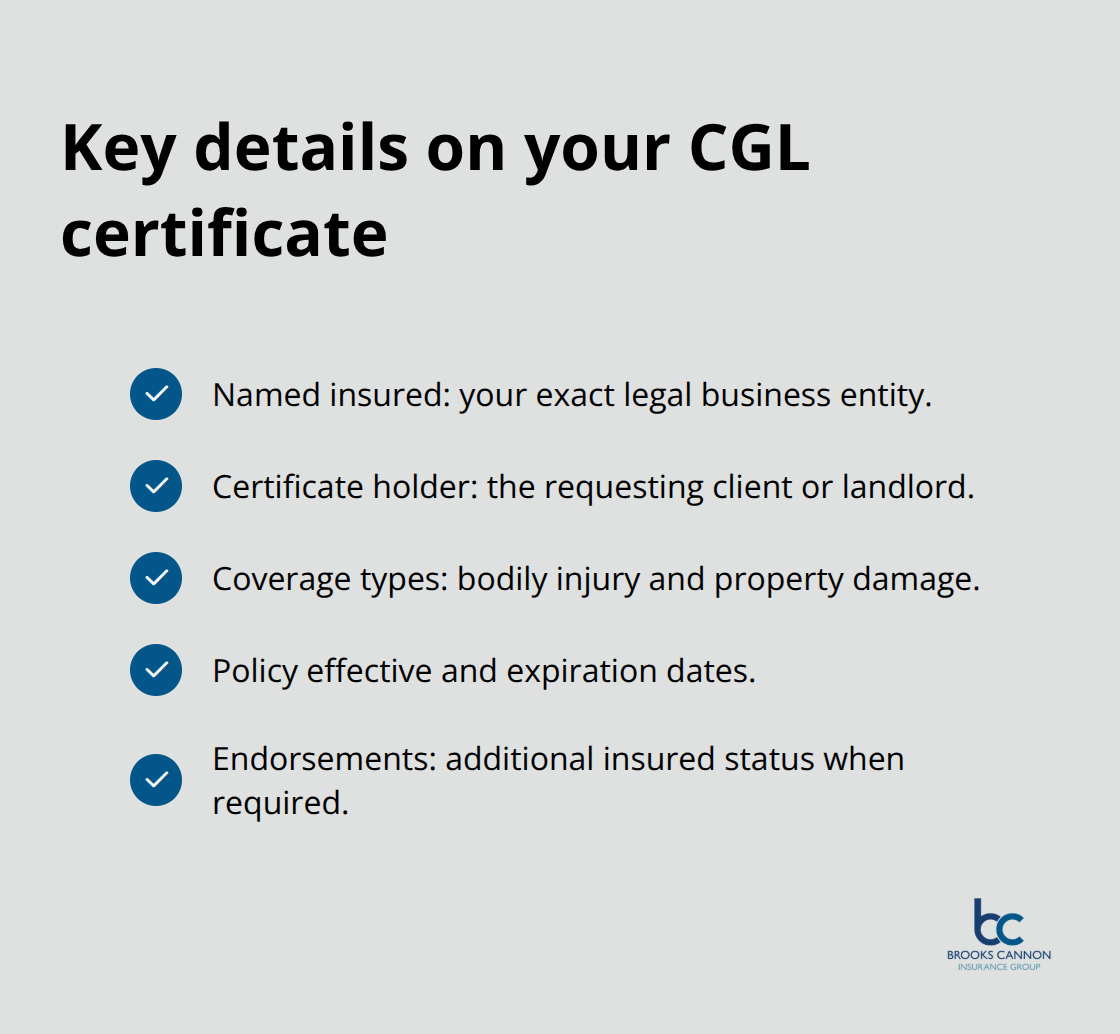

What Information Appears on Your Certificate

Your certificate lists the named insured (your business name), the certificate holder (whoever requested the certificate), coverage types like bodily injury and property damage, policy effective and expiration dates, and any endorsements such as additional insured status. Additional insured endorsements are critical in many contracts-they extend your coverage to protect the other party if they’re sued for something your business caused. For example, a landlord often requires additional insured status, meaning if a customer slips in your leased space and sues the landlord, your policy covers the landlord’s defense costs. You should verify that your certificate matches your actual policy limits and includes any endorsements your contracts require.

If the certificate contains errors or outdated information, request a corrected version immediately, because an inaccurate certificate can create coverage gaps or contractual disputes later.

How to Move Forward With Your Certificate

Once you understand what your certificate contains and why partners need it, the next step involves taking action to obtain one. Your insurer or agent can walk you through the process, answer questions about your specific coverage, and address any endorsement requirements your contracts demand.

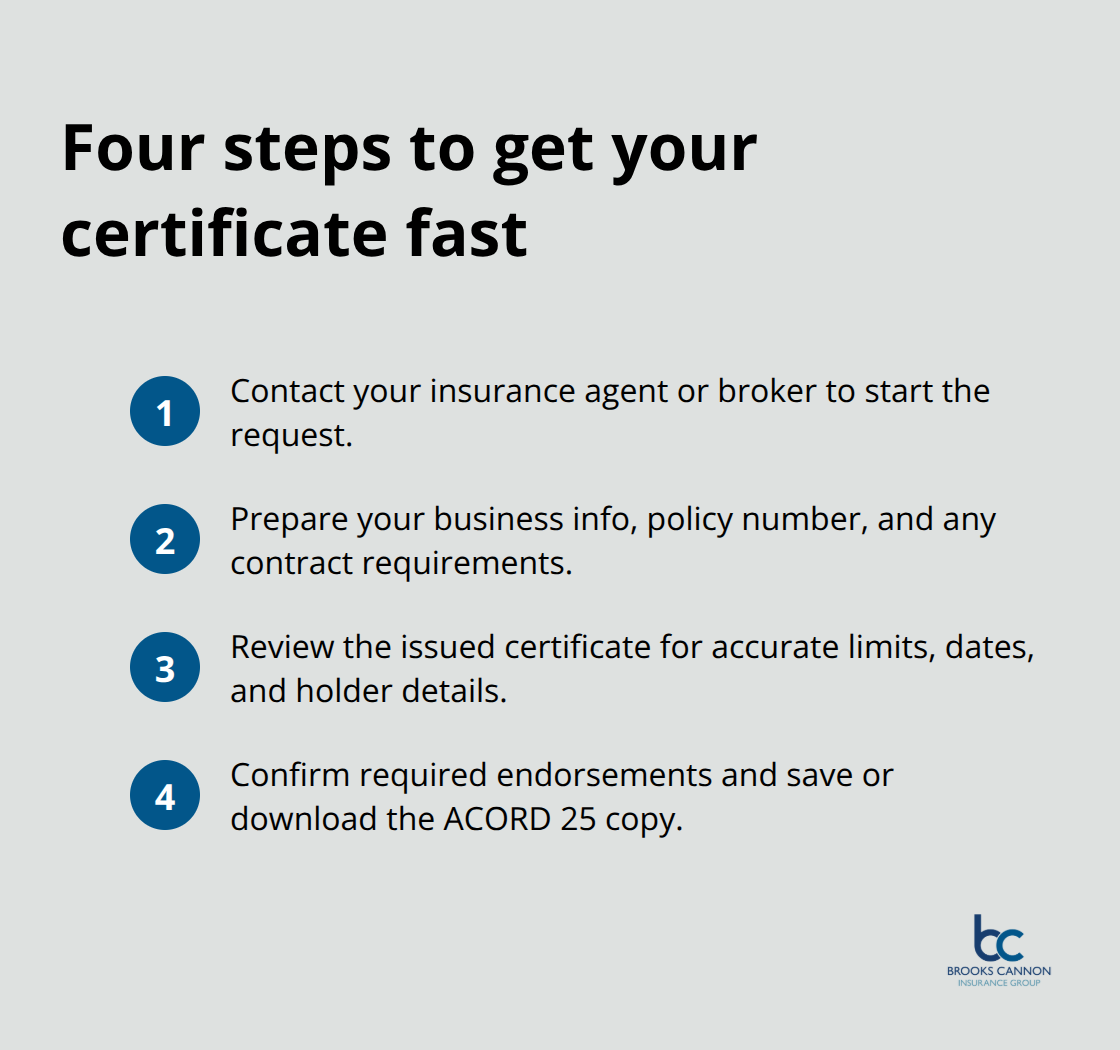

Getting Your Certificate in Four Steps

Start With Your Insurance Agent or Broker

Obtaining your certificate of commercial general liability insurance moves quickly when you know what to expect. Contact your insurance agent or broker directly to launch the process. If you already carry general liability coverage, your insurer generates a certificate within hours, and many carriers now offer online access to download it instantly from your policy dashboard. If you lack a policy, your agent guides you through selecting appropriate coverage limits based on your industry and contract requirements.

Dallas businesses face specific demands from clients and landlords regarding coverage amounts. A typical small Dallas retailer carries general liability limits around $1 million per occurrence and $2 million aggregate, though contractors and service providers frequently need higher limits depending on project scope and client contracts.

Prepare Your Information and Requirements

Have your business name, policy number, and any contract requirements ready when you contact your insurer or agent. Provide details about who needs the certificate, what coverage types they require, and whether additional insured endorsements apply to your situation. Many Dallas projects require certificates within 24 hours to meet bid deadlines, so communicating urgency helps your agent prioritize your request.

Ask your agent to confirm that the certificate includes all endorsements your contracts demand, particularly additional insured status if you work with landlords or larger clients. Additional insured endorsements add another party to your liability insurance policy to protect them if they face a lawsuit for something your business caused.

Review Your Certificate for Accuracy

Check the certificate details against your actual policy once you receive it. Verify that coverage limits match, effective dates align with your project timeline, and the certificate holder information appears with correct spelling. Errors on certificates create friction during contract negotiations and can delay project starts.

Request a corrected version immediately if you spot discrepancies. Most insurers issue certificates at no cost, and independent agencies with strong carrier relationships can often deliver them same-day through online systems. This speed eliminates delays that could cost you contracts or leases in competitive Dallas markets.

Understand What Your Certificate Contains

Your certificate lists the named insured (your business name), the certificate holder (whoever requested the certificate), coverage types like bodily injury and property damage, policy effective and expiration dates, and any endorsements such as additional insured status. The standard form used across the industry is called ACORD 25, which most insurers issue to policyholders at no charge. The Texas Department of Insurance maintains a registry of certificates, providing an official resource for verification.

Once you have your certificate in hand and verified its accuracy, you’re positioned to meet contractual demands and move forward with client relationships. The next step involves understanding what specific requirements different types of contracts and partnerships place on your certificate documentation.

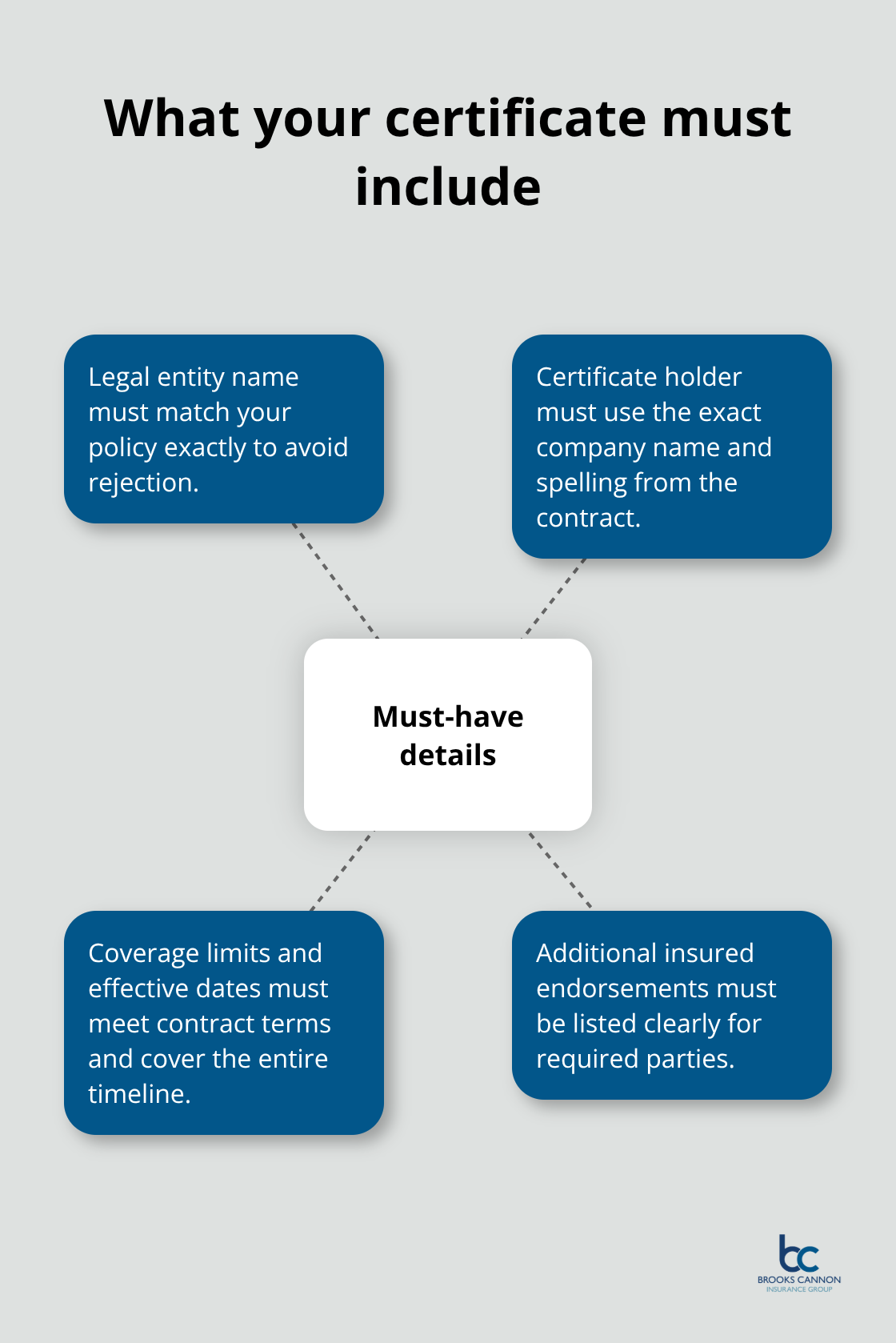

What Your Certificate Must Include

Match Your Legal Entity Name Exactly

Certificates of commercial general liability insurance aren’t one-size-fits-all documents. Different clients, landlords, and project managers require specific information on your certificate to satisfy their contractual and risk management needs. Your named insured information must match your actual business entity exactly as it appears on your policy. If you operate as an LLC, S-corp, or sole proprietorship, the certificate shows your legal entity name, not a doing-business-as name or nickname. This mistake appears frequently-a business owner uses a trade name on their certificate while their policy lists their legal entity differently, creating confusion and sometimes forcing clients to reject the certificate outright.

Identify the Certificate Holder Correctly

The certificate holder section identifies who requested the certificate, which is typically your client, landlord, or the general contractor on a project. This field must include the exact company name and spelling provided in your contract, because mismatches create unnecessary back-and-forth with contract administrators who need assurance they’re listed correctly. A single typo or abbreviation difference can trigger rejection and delay your project start.

Align Coverage Limits and Effective Dates With Your Contract

Coverage limits and effective dates are non-negotiable requirements that must align with your contract demands. If your contract requires $1 million per occurrence and $2 million aggregate, your certificate must reflect those exact limits or your client will reject it. Effective dates need to cover your entire project timeline-if your certificate expires before your work finishes, you’ll need a renewal certificate well in advance. Many Dallas projects operate on tight schedules, so planning ahead prevents last-minute scrambles for updated certificates.

Add Additional Insured Endorsements When Required

Additional insured endorsements extend your liability coverage to protect another party if they face a lawsuit related to your work. Most Dallas landlords require additional insured status, meaning if a customer is injured in your leased space and sues the landlord, your insurance covers the landlord’s legal defense. Contractors and subcontractors working on larger projects almost always demand additional insured status from their vendors and subcontractors. The certificate must clearly show the additional insured endorsement with the correct entity name, because vague language like “as per contract” leaves room for disputes if a claim arises. Contact your agent to confirm all endorsements before the certificate is issued, since corrections require reissuing the document and can delay your project start by days.

Final Thoughts

Getting your certificate of commercial general liability insurance in place removes a major barrier to winning contracts and leasing commercial space in Dallas. The process itself is straightforward: contact your agent, provide your contract requirements, review the certificate for accuracy, and submit it to whoever requested it. Most insurers deliver certificates within hours, and many offer online access so you can download and share them instantly.

The real protection comes from the actual insurance behind the certificate. Your general liability policy covers third-party bodily injury and property damage claims that could otherwise devastate your business, and a single lawsuit can cost $15,000 or more in legal fees alone. Without coverage, that expense comes directly from your business bank account, which is why having the right policy matters far more than the certificate itself.

We at Brooks Cannon Insurance Group work with Dallas business owners every day to build insurance programs that match their actual risks. Whether you need a certificate of commercial general liability insurance for a single project or a comprehensive insurance package that covers general liability, property, workers’ compensation, and cyber risks, our team understands the Dallas market and what your contracts demand.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation