Cyber liability insurance cost varies dramatically depending on your business type, size, and security practices. Most Dallas business owners underestimate how much they’ll actually pay when a breach happens.

At Brooks Cannon Insurance Group, we’ve seen too many companies shocked by hidden deductibles and coverage gaps that leave them exposed. This guide breaks down exactly what you’ll pay and where the real expenses hide.

What Moves Your Cyber Liability Premium

Your cyber insurance premium isn’t pulled from thin air. Insurers calculate it based on concrete risk factors they measure carefully. Understanding these drivers helps you control costs instead of accepting whatever quote lands on your desk.

Industry risk shapes your baseline cost

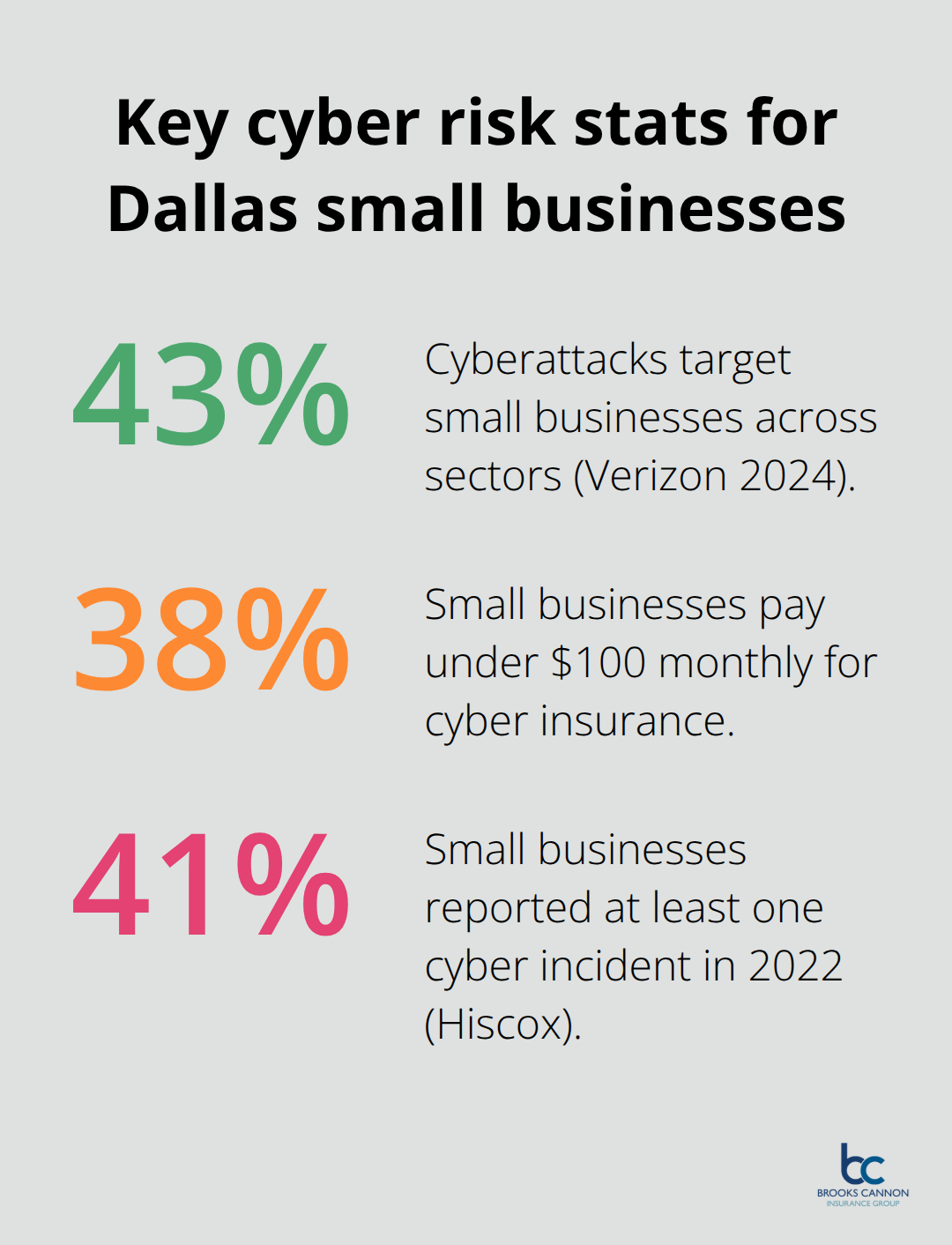

Healthcare providers, financial institutions, and tech companies pay significantly more than construction firms or real estate agencies. TechInsurance data shows that industry risk matters because certain sectors face higher attack frequencies and steeper regulatory penalties. A healthcare startup handling patient records might pay $5,000 to $10,000 annually, while an IT consultant with similar company size could pay $2,500 to $6,000. This isn’t arbitrary. Healthcare data breaches trigger HIPAA fines up to $1.5 million per violation, so insurers charge accordingly. Finance and insurance companies face similar scrutiny. If you operate in manufacturing, energy, or utilities, expect higher premiums than industries with less sensitive data exposure. The Verizon 2024 Data Breach Investigations Report found that 43% of cyberattacks target small businesses across all sectors, but the financial consequences differ wildly by industry.

Company size and revenue determine your price tier

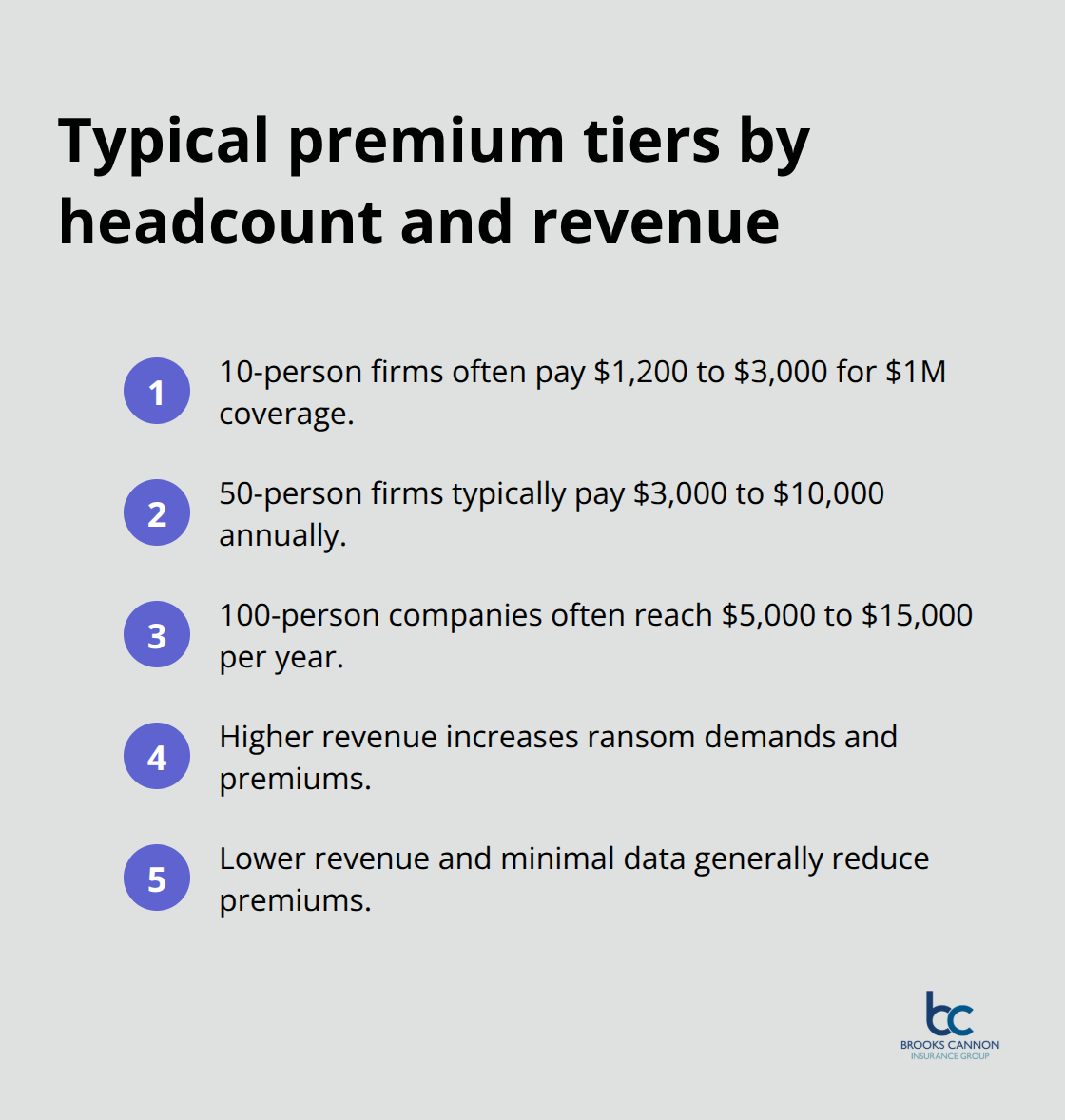

A 10-person consulting firm pays roughly $1,200 to $3,000 annually for $1 million in coverage.

A 50-person firm typically pays $3,000 to $10,000. A 100-person company often reaches $5,000 to $15,000. The relationship is nearly linear because more employees mean more entry points for attackers, more data stored, and higher potential settlement costs. Your annual revenue also factors in. Attackers demand larger ransoms from profitable companies. A startup generating $500,000 in revenue faces lower premiums than one doing $5 million. Insurers view revenue as a proxy for the size of potential extortion demands and the resources available for recovery.

Security maturity either saves you money or costs you dearly

This is where you control your destiny. Companies with multi-factor authentication, encrypted data storage, regular security audits, and documented incident response plans receive meaningful discounts from insurers. A business with weak security controls pays full price or faces rejection entirely. If you implement MFA on critical accounts, maintain a firewall, conduct annual phishing training, and keep systems patched, insurers typically reward this with 10% to 25% premium reductions. A company that minimizes data collection and uses tokenization to avoid storing sensitive information outright reduces both risk and premium. IBM research shows that organizations with strong automation and incident response plans contain breaches in an average of 200 days versus 308 days for unprepared companies, saving roughly $1.8 million per incident. Insurers see this data and price accordingly.

What Dallas businesses actually pay

The real cost breakdown depends on how these three factors combine for your specific operation. A small Dallas firm with basic security controls and low-risk data might pay $1,200 to $2,500 annually. The same firm with robust security measures could drop that to $900 to $1,800. A mid-market company in a regulated industry without strong controls could hit $8,000 to $12,000, while one with mature security practices might stay at $5,000 to $8,000. These ranges matter because they show you where your leverage sits. Poor security practices are expensive. Dallas business owners who invest in prevention spend less on insurance and gain real protection against the threats that actually target your industry and size.

Real Cost Breakdown for Dallas Businesses

Small businesses pay annually for cyber liability coverage

Small Dallas businesses with fewer than 50 employees typically pay an average premium of $145 per month, or about $1,740 annually for cyber liability coverage. A 10-person firm with minimal data storage and basic security controls lands around the lower end of this range, while a 40-person firm with more extensive client information and stronger security practices pays toward the higher end. The difference hinges on what you store and how you protect it.

If you handle credit card numbers, client names, or employee tax information, expect higher premiums. If you run a service business with limited data exposure, you’ll pay less. Deductibles typically run $2,500 for policies at this coverage level, meaning your out-of-pocket cost in a breach reaches that amount before insurance kicks in.

About 38 percent of small businesses pay under $100 monthly for cyber insurance. This coverage usually covers only first-party costs like forensics and notification expenses, not third-party liability if customers sue you.

Mid-market companies face $5,000 to $15,000 annually

Mid-market Dallas companies with 50 to 200 employees usually carry $2 million to $5 million in coverage and pay $5,000 to $15,000 annually. Industry and security posture drive the variation significantly. A manufacturing firm with 75 employees and moderate data collection might pay $6,000 to $9,000, while a financial services firm of similar size handling sensitive customer data could reach $12,000 to $15,000.

Healthcare providers in this range almost always exceed $10,000 because regulatory exposure is severe. The critical insight here is that security maturity compresses costs across all size ranges. A mid-market firm that implements multi-factor authentication, maintains quarterly security audits, and documents incident response procedures can reduce premiums by 15 to 25 percent compared to peers without these controls.

Enterprise operations pay $15,000 to $25,000 or more

Enterprise-level Dallas operations with 200+ employees and significant data volumes typically pay $15,000 to $25,000 or higher annually for $5 million to $10 million in coverage. A tech company with 150 employees handling client infrastructure faces different pricing than a manufacturing firm of the same size.

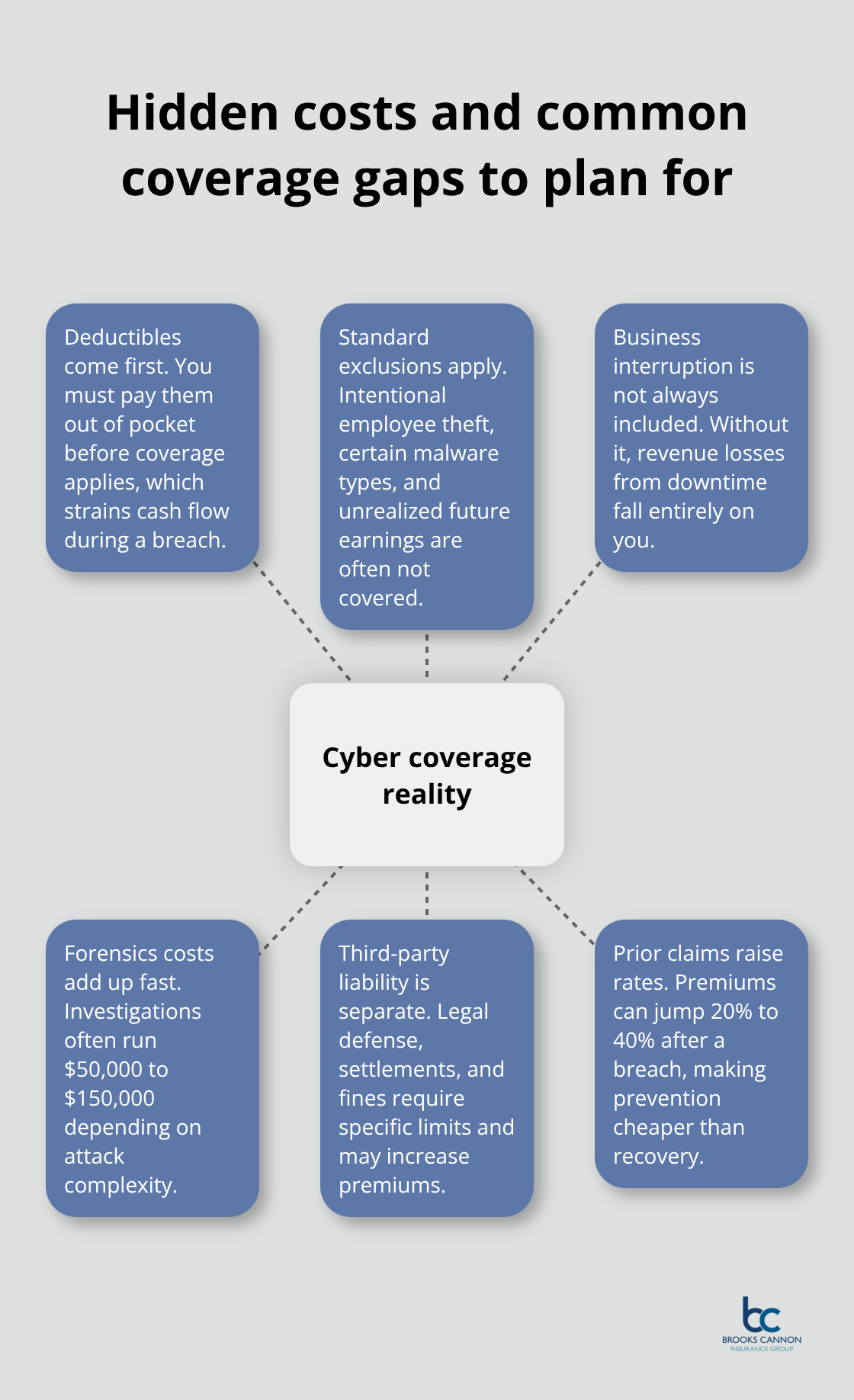

Prior cyber claims hit your wallet hard on renewal. A company that suffered a previous breach typically sees premiums jump 20 to 40 percent, making prevention far cheaper than recovery. This penalty structure creates a powerful incentive to invest in security controls now rather than pay inflated rates later.

The gap between a well-protected company and one with weak defenses widens as your organization grows. What separates affordable coverage from expensive policies isn’t just your industry or size-it’s whether you’ve taken concrete steps to reduce your actual risk. Understanding what triggers these cost differences helps you identify where to focus your professional liability insurance investments for maximum impact on your bottom line.

Hidden Costs and Coverage Gaps to Watch

Deductibles create immediate out-of-pocket expenses

Your cyber insurance policy includes a deductible that you pay before the insurance company covers anything. A $2,500 deductible sounds manageable until you’re in the middle of a breach response and realize you’re writing a check before the insurance company writes theirs. TechInsurance data shows that common deductibles sit around $2,500 for $1 million in coverage, but you can negotiate higher deductibles to lower your premium. Choosing a $25,000 deductible instead of $2,500 might reduce your annual premium from $4,000 to $1,800, but that trade-off only makes sense if your business can absorb that out-of-pocket hit without crippling operations.

Small Dallas firms with tight cash flow should stick with lower deductibles even if premiums cost more. A breach happens when your finances are already strained, and a large deductible forces you to fund recovery from your operating account. The math is simple: pay slightly more monthly to avoid a catastrophic bill when you need liquidity most.

Standard policies exclude critical scenarios

Your cyber policy isn’t a safety net that catches everything. Standard cyber policies exclude losses from intentional employee theft, future earnings you didn’t generate yet, and certain malware types depending on the policy language. These gaps matter because they shift costs back to you.

A ransomware attack that disrupts your operations for three weeks creates lost revenue that insurance won’t cover if your policy lacks business interruption coverage.

You also won’t recover costs from social engineering attacks where an employee was tricked into transferring funds, even though the Hiscox Cyber Readiness Report 2023 found that 41% of small businesses reported at least one cyber incident in 2022, with many involving employee error. Review your policy exclusions section before you face a crisis and learn which scenarios leave you exposed.

Business interruption costs drain your recovery budget

When your systems go down, every hour costs money through lost sales, missed client deadlines, and employee downtime you still have to pay. First-party cyber coverage pays for forensic analysis to identify what happened and how to prevent it again, typically running $50,000 to $150,000 depending on attack complexity. If your policy doesn’t include business interruption coverage, you absorb revenue losses entirely.

A Dallas e-commerce business losing $5,000 daily during a three-week recovery faces $105,000 in losses that insurance won’t touch without explicit business interruption limits. Third-party coverage adds another layer by paying legal fees, settlements, and regulatory fines when customers sue you over a data breach, but this coverage costs more and isn’t standard in all policies.

Total breach costs exceed what most policies cover

IBM’s 2023 Cost of a Data Breach Report showed the average total cost of a data incident in the U.S. reaches $9.48 million, with breach containment, notification, legal defense, and regulatory penalties all stacking up quickly. Your policy might cover notification costs but cap them at $50,000 when your actual liability exposure is far higher. Request detailed quotes that specify what’s included for forensics, notification expenses, crisis management, and business interruption, then calculate what a realistic breach scenario would cost your operation (forensics, legal defense, customer notification, and lost revenue combined). That calculation reveals whether your coverage limits match your actual exposure or whether you’re gambling with underinsurance.

Final Thoughts

Cyber liability insurance cost depends on three factors you control: your industry, company size, and security practices. Dallas business owners who audit their security controls, calculate realistic breach costs, and compare quotes from multiple carriers stop overpaying and start protecting what matters. Multi-factor authentication, data encryption, regular security audits, and documented incident response plans reduce your actual risk and trigger meaningful premium discounts from insurers.

Contact Brooks Cannon Insurance Group to discuss your cyber liability needs and receive quotes tailored to your Dallas operation. Our licensed experts review your data handling practices, regulatory obligations, and current security measures, then match you with policies that protect against real threats without paying for unnecessary coverage. We handle the complexity so you can focus on running your business.

Getting a customized quote takes less time than you think. We’ll explain what each policy covers, identify coverage gaps, and show you where security investments reduce both risk and premium. Your cyber liability insurance cost should match your actual exposure, not a generic estimate.