Owning rental property in Dallas comes with real financial exposure. Standard homeowners policies leave landlords vulnerable to gaps that can cost thousands when tenant disputes or property damage occur.

We at Brooks Cannon Insurance Group work with local landlords every day who discover these gaps too late. This guide walks you through the Dallas landlord coverage options that actually protect your investment.

Why Standard Homeowners Policies Fail Rental Properties

A standard homeowners policy is designed for owner-occupied homes, not rental investments. When you rent out a property in Dallas, your insurer views the risk profile completely differently. The moment tenants move in, your policy either excludes rental activity altogether or provides such limited coverage that you remain essentially unprotected. We at Brooks Cannon Insurance Group see this problem repeatedly: landlords face coverage denials only after a tenant injury or property damage claim occurs. The Texas Department of Insurance reports that many homeowners policies explicitly exclude or severely limit coverage for damage or liability arising from rental activities, which means you could face tens of thousands in unexpected costs.

The Real Cost of Rental Exclusions

A standard homeowners policy typically does not cover liability if a tenant or their guest is injured on the property. If someone slips on your stairs and files a lawsuit, your homeowners policy won’t defend you. Similarly, if a tenant’s carelessness causes a fire that damages the structure, coverage may be denied because the policy treats rental properties as a higher-risk category. Property damage from tenant disputes, broken appliances, or water damage from negligence often falls into coverage gaps as well.

Dallas landlords operate in Texas under landlord-friendly laws, but insurance protection still depends on having the right policy type. A dwelling fire policy, often called DP-3, is specifically designed for rental properties and costs more than a standard homeowners policy because rental properties statistically generate more claims. According to TGS Insurance Agency, the typical Texas average for landlord insurance runs about $1,320 per year, though Dallas properties often cost more due to local hail and wind risk.

What Landlord-Specific Coverage Actually Protects

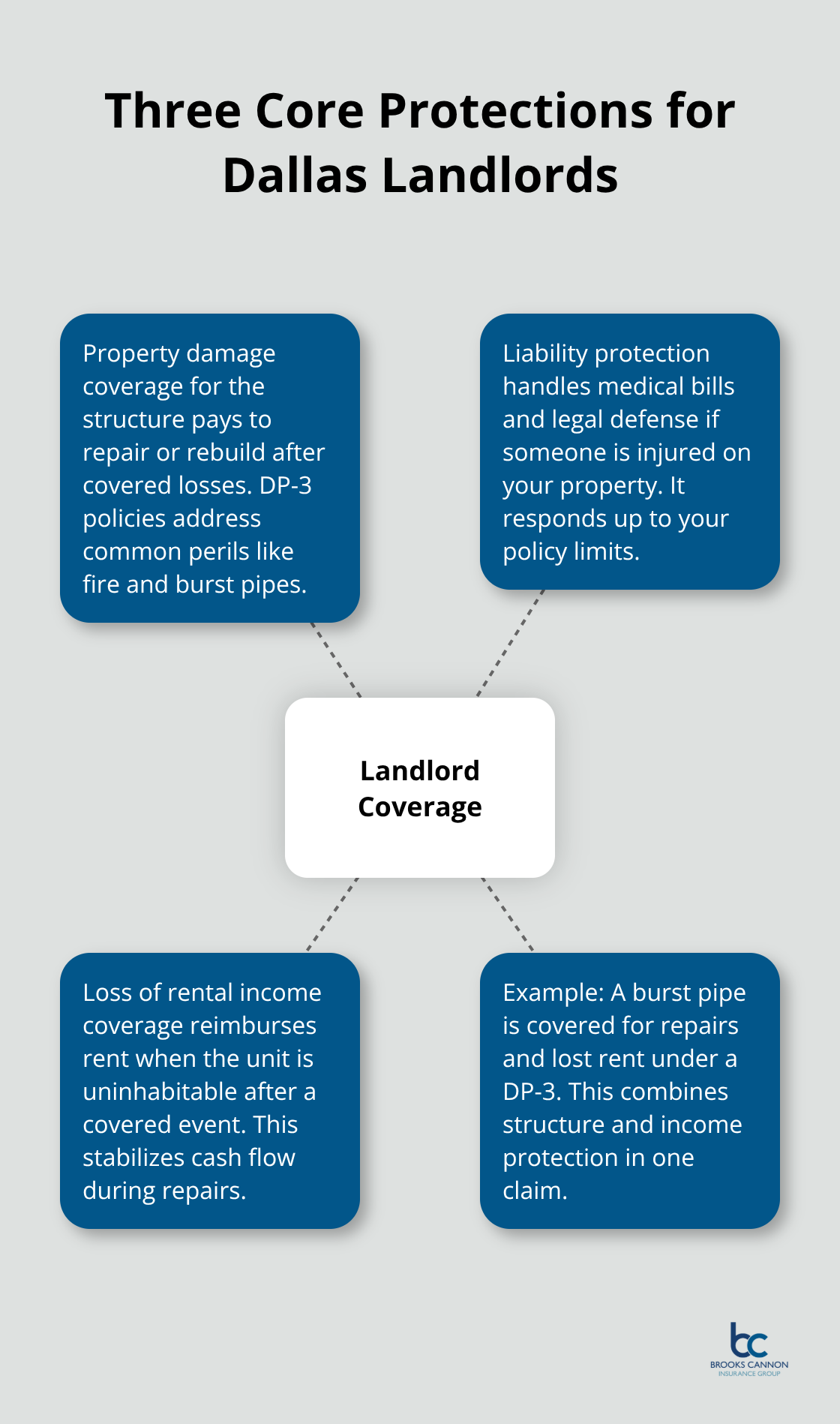

Landlord-specific coverage includes three core protections that homeowners policies skip entirely: property damage coverage for the structure, liability protection if someone is injured on your property, and loss of rental income coverage if the property becomes uninhabitable. If a burst pipe damages your rental unit, a DP-3 covers the repair costs and reimburses you for rent you lose while repairs happen. If a tenant’s guest is injured and sues, your liability coverage handles medical bills and legal fees up to your policy limits.

Most Dallas landlords should carry at least $500,000 in liability coverage, though experienced investors often choose $1,000,000 for stronger protection. Roof age matters significantly in Dallas: carriers typically require roofs under 15 years old for full replacement-cost coverage, and roofs older than 20 years may only be covered on an actual cash value basis or trigger higher deductibles.

Policy Types and What They Cover

Choosing the right dwelling fire policy type matters significantly. A DP-1 policy uses actual cash value and covers only named perils, making it the cheapest option but leaving gaps. A DP-2 adds more covered perils and pays replacement cost value. A DP-3 is open-peril with replacement cost, offering the broadest protection and the coverage most lenders require for rental properties in Dallas. Understanding these distinctions helps you select coverage that matches both your property’s risk profile and your financial situation.

Essential Coverage Types for Dallas Rental Properties

Dwelling Fire Insurance and Replacement-Cost Protection

Dwelling fire insurance, commonly called DP-3, forms the foundation of protection for Dallas rental properties and differs fundamentally from the DP-1 or DP-2 options. A DP-3 policy covers the structure on a replacement-cost basis, meaning your insurer pays what it actually costs to rebuild or repair after a covered loss, not the depreciated value. This matters enormously in the Dallas-Fort Worth market, where construction costs have risen steadily. If your rental property suffers fire damage, a burst pipe, or storm damage, replacement-cost coverage rebuilds the structure at current market prices rather than leaving you short.

You should try for dwelling coverage that equals 100 percent of your property’s replacement cost, not its market value. Many Dallas landlords underestimate this figure and end up underinsured. Review your coverage limits annually to keep pace with Dallas-Fort Worth construction cost increases, since inflation can quickly erode your protection.

Extended Protection for Water and Other Structures

DP-3 policies include coverage for other structures on your property, such as detached garages, storage sheds, and fences. Extended protection riders add coverage for water backup, which is particularly valuable in Texas where water damage claims are common and carriers frequently cap standard water damage coverage at $10,000. Request removal of water-damage limits if your carrier allows it, since a single water event can easily exceed that threshold. Water damage from burst pipes and appliance overflow represents one of the most frequent claims Dallas landlords file, making this protection essential.

Liability Coverage for Tenant and Visitor Injuries

Liability coverage protects you when a tenant or visitor is injured on your property and holds you responsible. Texas premises liability law requires landlords to maintain conditions affecting health and safety, and adequate liability coverage handles both the legal defense and any settlements or judgments. Start with at least $300,000 in liability coverage, though most Dallas landlords benefit from $500,000 to $1,000,000 in protection. This coverage pays medical bills, attorney fees, and court settlements up to your policy limits if someone sues after a slip-and-fall, dog bite, or other injury incident.

Loss of Rents Coverage During Property Repairs

Loss of rents coverage reimburses you for rental income lost when the property becomes uninhabitable due to a covered event. If a fire or burst pipe makes the unit unlivable and you must move tenants out, this coverage typically pays your lost rent for up to 12 months while repairs occur. This protection stabilizes cash flow during recovery and prevents you from carrying mortgage payments on a non-income-producing property. Calculate your monthly rent and set your loss-of-rents limit to cover a reasonable claim period-many landlords set this limit too low, then face significant out-of-pocket losses if repairs take longer than expected.

Choosing the Right Coverage Limits for Your Situation

Your specific coverage needs depend on your property’s replacement cost, the number of tenants, and your financial capacity to absorb losses. Properties in Dallas with higher hail and wind risk typically command higher premiums than statewide averages, so factor this into your budget. Roof age significantly influences your rates and coverage options: carriers typically require roofs under 15 years old for full replacement-cost coverage, while roofs older than 20 years may only be covered on an actual cash value basis or trigger higher deductibles. Understanding these variables helps you select protection that matches both your property’s risk profile and your financial situation, positioning you to make informed decisions about additional coverage options.

Selecting Coverage That Matches Your Property and Risk Profile

Calculate Your Dwelling Coverage Based on Replacement Cost

Start by documenting exactly what you own and what tenants occupy. Walk through your rental property and note the replacement cost of the structure itself, not its market value. In Dallas, construction costs typically run around $120 per square foot for standard residential rebuilds, though this varies by neighborhood and property condition. Multiply your square footage by these figures to estimate replacement cost, then add 20 percent as a buffer for inflation and unforeseen expenses. This number becomes your dwelling coverage limit.

Many Dallas landlords make the mistake of insuring based on what they paid for the property five years ago, then face severe underinsurance when a major loss occurs. If your property is worth $300,000 on the market but costs $400,000 to rebuild due to current labor and material costs, your coverage limit should be $400,000, not $300,000. An honest assessment of your property’s actual risk profile ensures you avoid generic coverage limits that sound adequate but leave gaps when claims arise.

Assess Roof Age and Its Impact on Coverage

Roof age directly influences both your premium and your coverage eligibility. Carriers typically require roofs under 15 years old for full replacement-cost coverage; if your roof is between 15 and 20 years old, expect higher deductibles or actual cash value limitations; if your roof exceeds 20 years, many carriers apply actual cash value only or refuse coverage entirely.

Request a roof inspection report from a qualified contractor before you shop for quotes. This document proves age and condition to underwriters and often unlocks better rates. Tenants matter significantly to your premium calculation. Single-family homes with one long-term tenant cost less to insure than multi-unit properties or short-term rentals. If you operate an Airbnb or VRBO, expect premiums roughly 50 to 80 percent higher than long-term rental rates because guest turnover increases property damage and liability exposure. Misrepresenting occupancy type to save money on premiums is one of the fastest ways to have claims denied, so disclose your actual rental model to your agent upfront.

Optimize Your Deductible and Coverage Limits

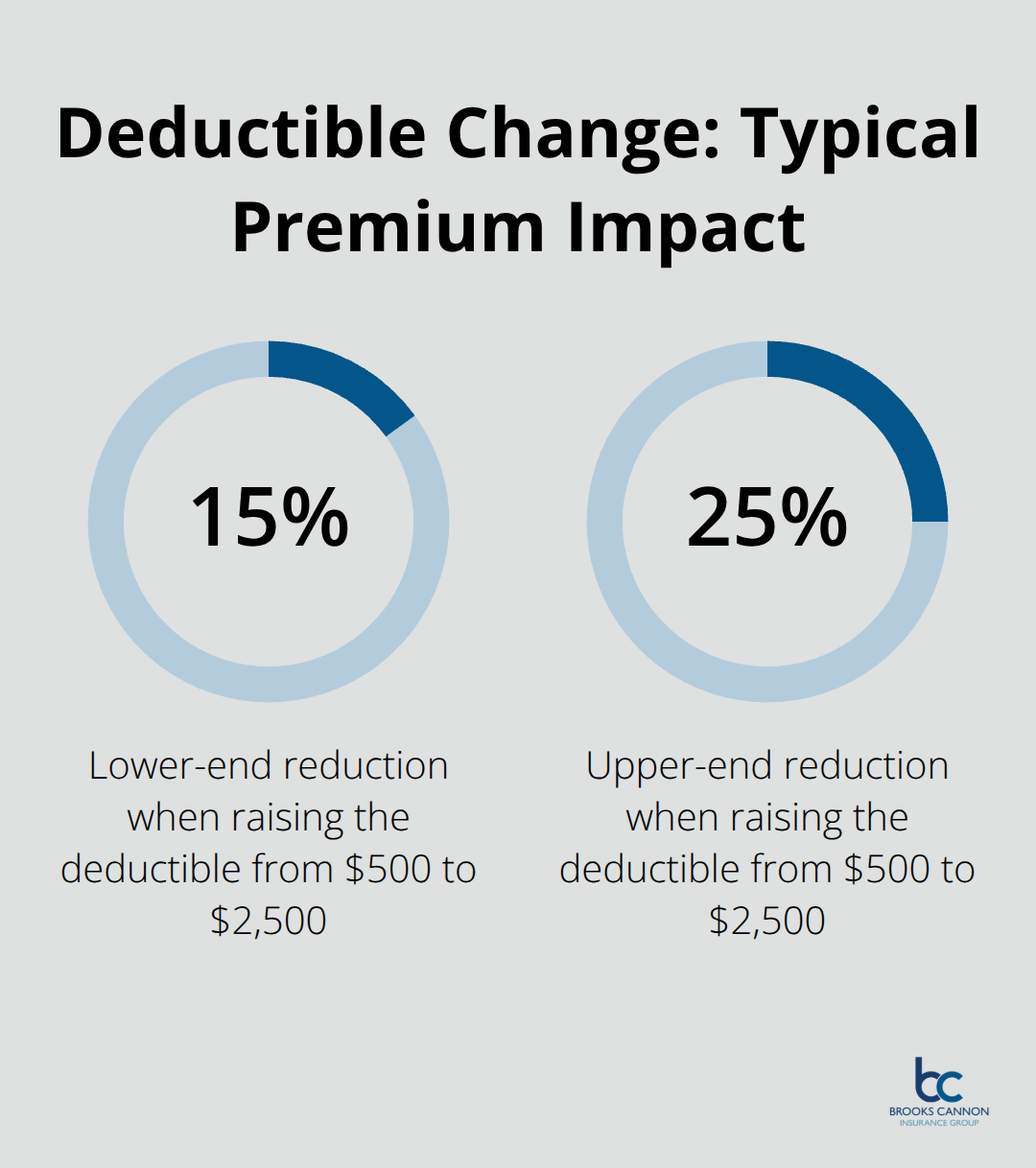

Deductible selection directly controls your premium. Raising your deductible from $500 to $2,500 typically reduces annual premiums by 15 to 25 percent, depending on your carrier and property. However, this only works if you actually have $2,500 available to cover losses out of pocket. Most experienced Dallas landlords choose $1,000 to $2,500 deductibles because the premium savings outweigh the occasional out-of-pocket cost.

Coverage limits deserve equal attention. Liability limits should start at $500,000 minimum for single-family rentals and $1,000,000 for multi-unit properties or properties in high-traffic areas. Loss of rents coverage should equal your monthly rent multiplied by 12 months as a baseline, since major repairs often take 6 to 12 months. If you charge $2,500 monthly rent, set your loss-of-rents limit to $30,000 minimum.

Water damage coverage must be examined carefully because standard policies frequently cap this at $10,000, which evaporates instantly with a single burst pipe claim. Request removal of water-damage limits entirely if your carrier permits it, or increase the limit to at least $50,000.

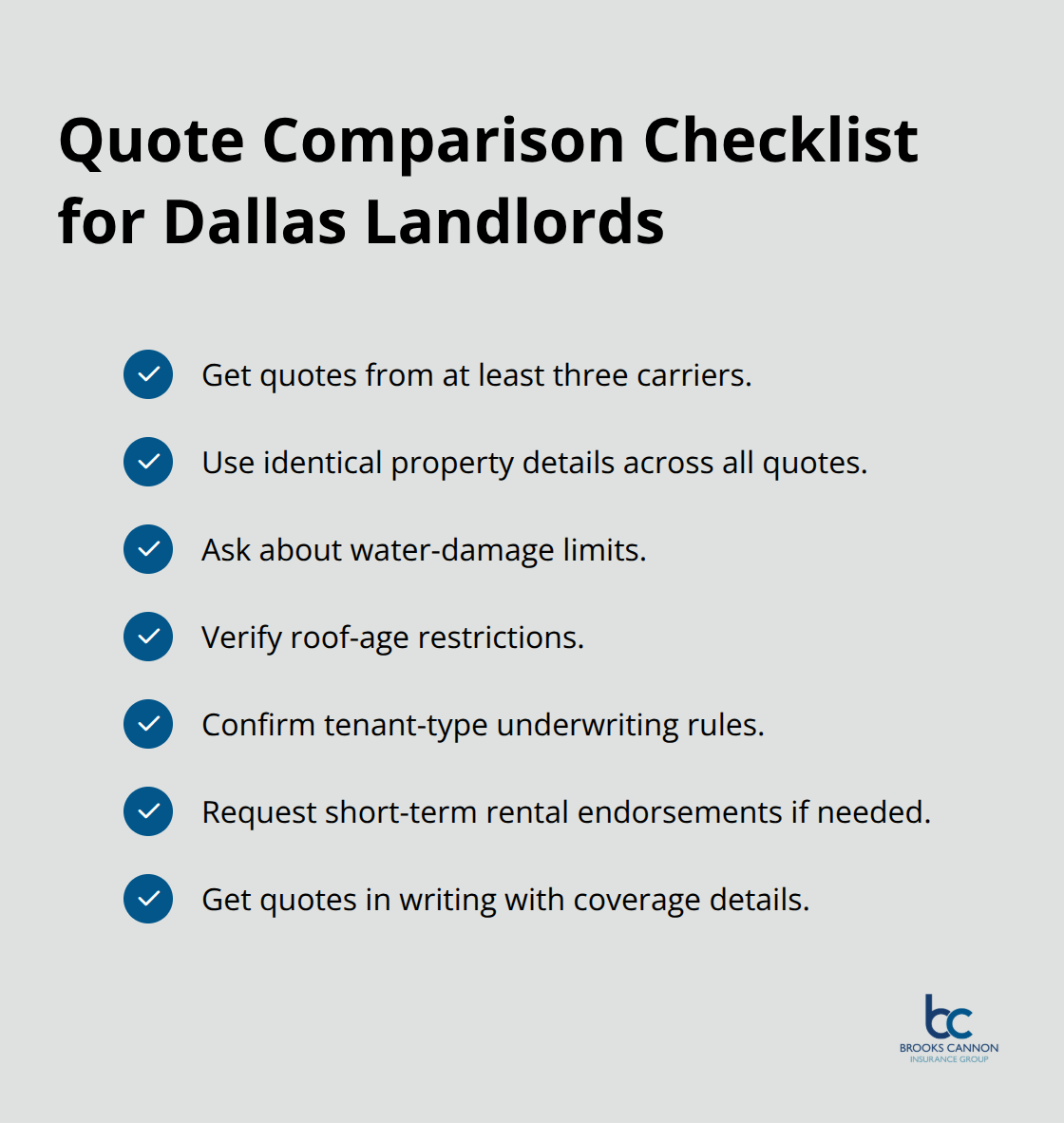

Compare Quotes Across Multiple Carriers

Work with an independent agent who evaluates your specific risk profile across multiple carriers to ensure you avoid paying for unnecessary coverage while maintaining adequate protection. An agent unfamiliar with Dallas hail patterns, wind exposure, and roof age restrictions may quote you with carriers that later deny claims or apply unexpected limitations.

Request quotes from at least three carriers using identical property details to compare actual premium differences across DP-1, DP-2, and DP-3 options. Ask each agent specifically about water-damage limits, roof-age restrictions, tenant-type underwriting, and whether short-term rental endorsements are available if you need them. Get quotes in writing with coverage details spelled out, not just a premium number, so you can compare apples to apples across carriers.

Final Thoughts

Dallas landlord coverage requires three non-negotiable protections: dwelling fire insurance on a replacement-cost basis, liability coverage starting at $500,000, and loss of rents coverage to stabilize cash flow during repairs. Without these three components, you expose yourself to catastrophic financial loss when tenant disputes or property damage occur. A DP-3 policy delivers all three protections in one package, making it the standard choice for Dallas rental properties.

Roof age, water damage limits, and tenant type directly influence both your premium and your coverage eligibility, so these factors demand careful attention during the quote process. Gather documentation about your specific property: square footage, roof age, current replacement cost, monthly rental income, and your actual tenant situation. Contact multiple carriers through an independent agent who understands Dallas market conditions, including local hail and wind exposure, and request written quotes comparing DP-1, DP-2, and DP-3 options with identical coverage details.

We at Brooks Cannon Insurance Group work with Dallas landlords every day to build coverage that actually protects their investments. Our licensed experts understand Dallas-specific risks, from hail damage to tenant-related liability claims, and we handle the comparison work so you receive comprehensive protection without overpaying. Contact us today to discuss your Dallas landlord coverage needs and receive a personalized quote that matches your property’s actual risk profile.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation