Being a landlord in Texas comes with real financial exposure. Property damage, tenant injuries, and liability claims can drain your savings fast.

Landlord insurance in Texas protects your investment and shields you from these risks. We at Brooks Cannon Insurance Group help property owners understand their coverage options and avoid costly gaps in protection.

What Landlord Insurance Actually Covers

How Landlord Insurance Differs from Homeowners Coverage

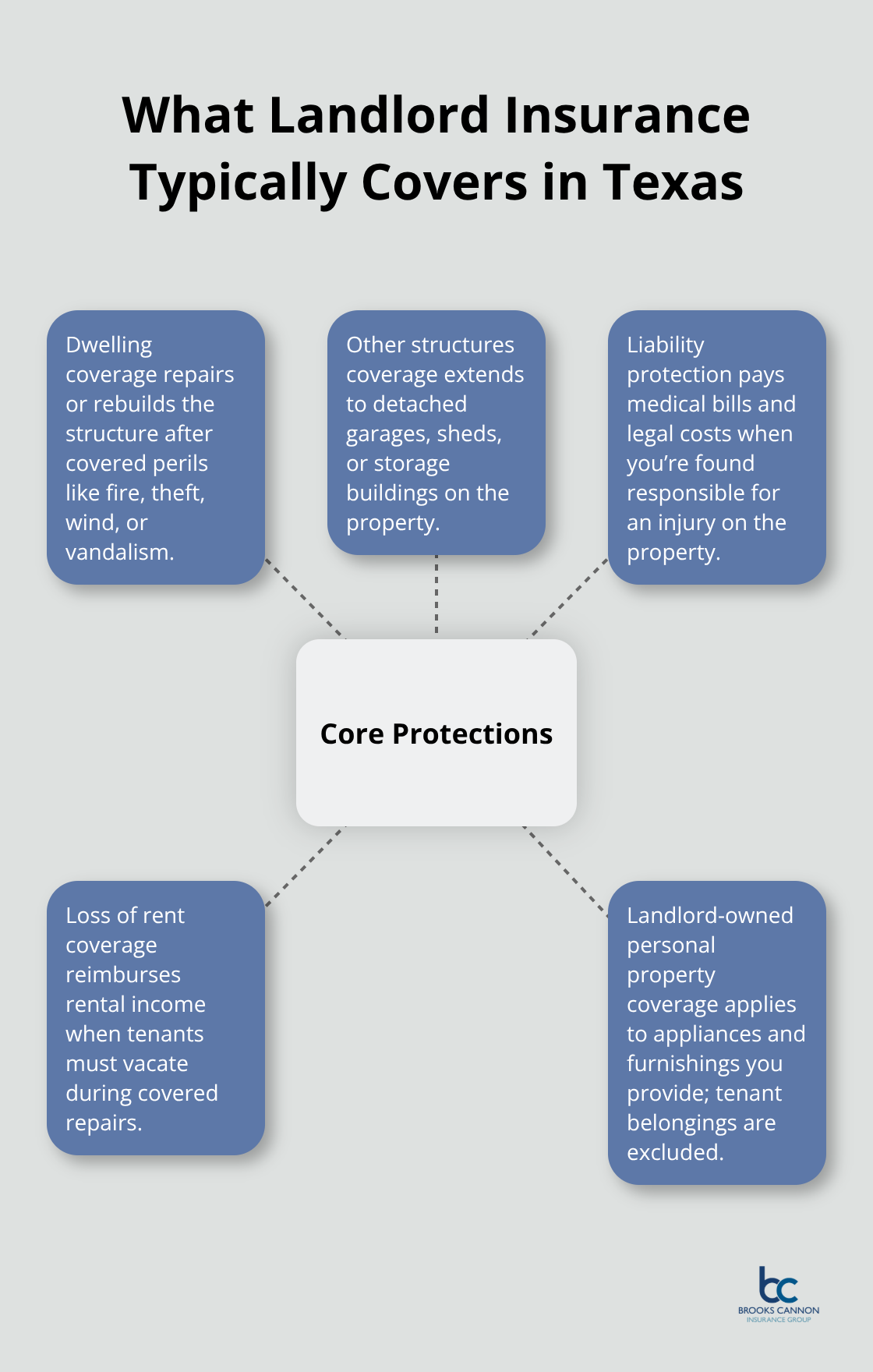

Landlord insurance in Texas is fundamentally different from homeowners insurance, and that distinction matters more than most property owners realize. Standard homeowners policies explicitly exclude rental properties, leaving you exposed if you attempt to use one for a rental unit. Landlord insurance fills that gap by protecting the structure itself through dwelling coverage, which pays for repairs or rebuilding after fire, theft, wind damage, or other covered perils. It also covers other structures on your property like detached garages or storage buildings. Landlord policies include liability protection that covers medical bills and legal costs if someone is injured on your property and you are found responsible. Loss of rent coverage separates smart landlords from those facing financial catastrophe-if a fire or storm forces tenants out temporarily, this coverage reimburses you for lost income while repairs happen.

From 1980–2024, Texas experienced 190 confirmed weather and climate disaster events with losses exceeding $1 billion each, making this income protection genuinely essential. Most policies also cover personal property you own inside units, such as appliances or furnishings you provide, though tenant belongings remain their responsibility to insure separately.

Regional Premium Variations Across Texas

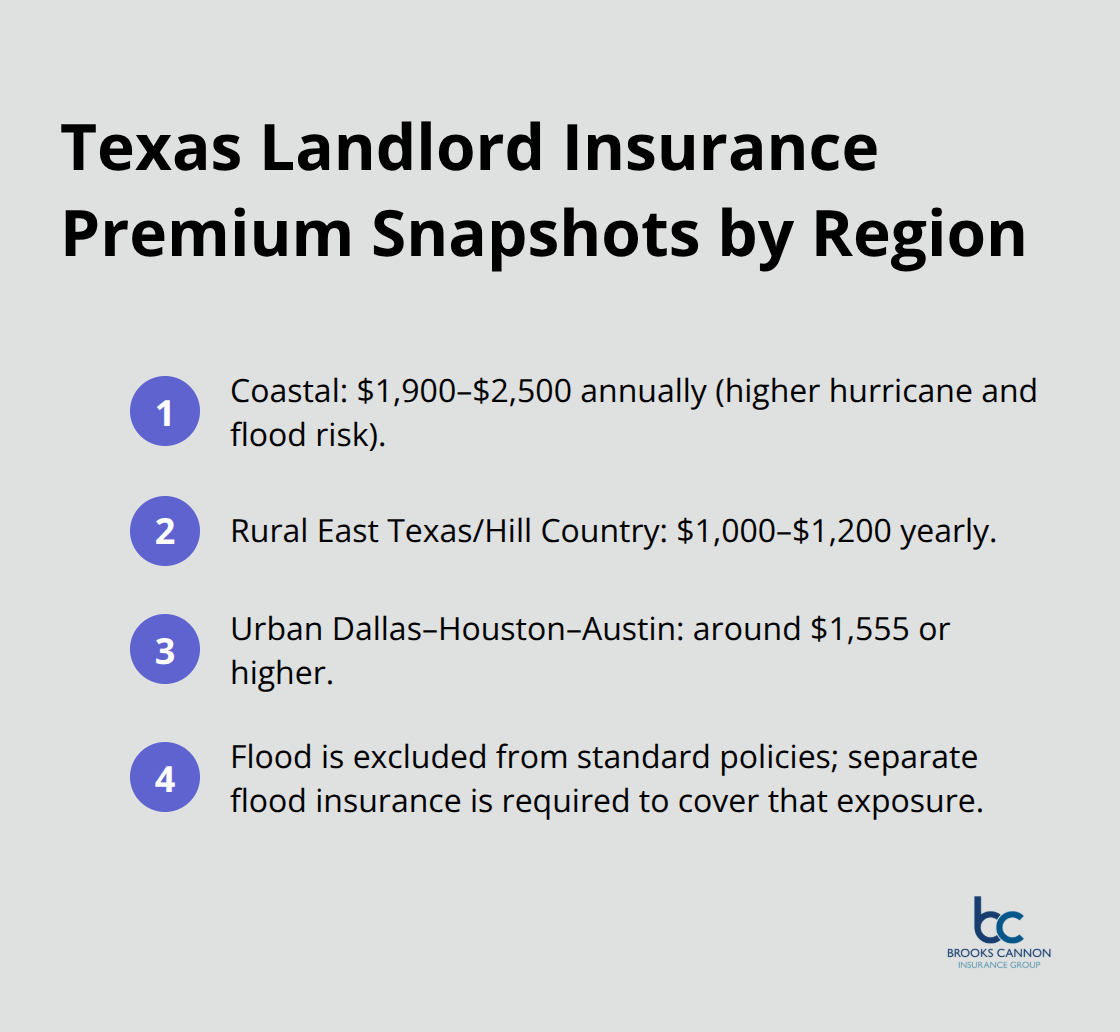

Texas creates specific insurance challenges that national averages simply do not capture. Coastal properties from Galveston to Corpus Christi face hurricane and flooding risks that drive premiums to $1,900 to $2,500 annually, while rural properties in East Texas or Hill Country typically run $1,000 to $1,200 yearly. Urban markets like Dallas, Houston, and Austin see premiums around $1,555 or higher due to higher property values and concentrated risk factors.

The Texas Flood Law requires you to inform tenants if a property sits in a flood zone or has sustained flood damage in the past five years, yet standard policies exclude flood damage entirely-you must purchase separate flood insurance to cover this exposure.

Natural Disaster Risks and Liability Exposure

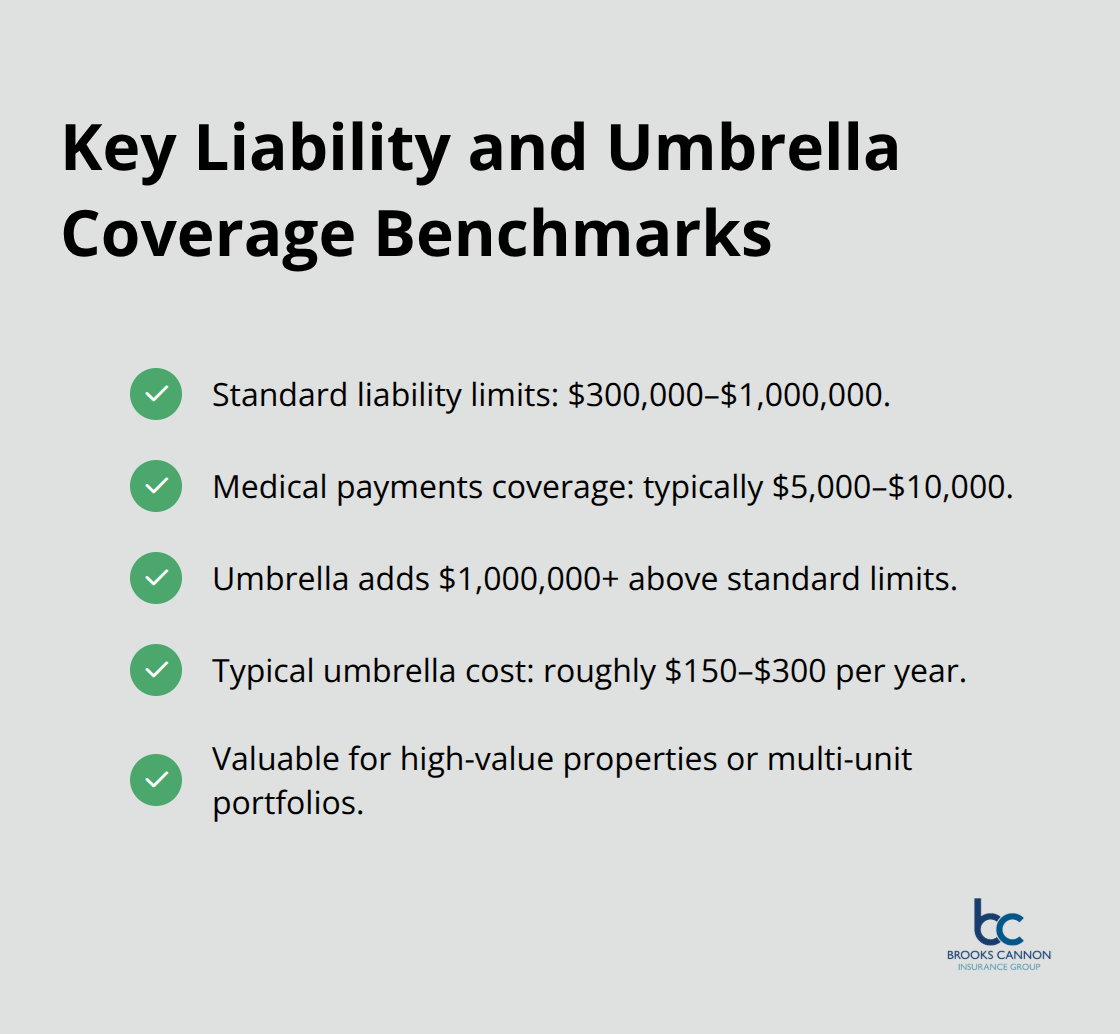

Hailstorms, tornadoes, wildfires, and sinkholes compound these risks across different regions of the state. Landlord liability exposure in Texas is substantial because someone injured on your property can pursue a claim regardless of whether you were directly negligent, making liability limits of $300,000 to $1,000,000 a practical necessity rather than an option. Legal requirements vary by lender; if you have a mortgage on the rental property, your lender almost certainly mandates landlord insurance as a loan condition, even though Texas law does not legally require it for unencumbered properties. This distinction means you cannot skip coverage simply because the state permits it-your financing agreement removes that choice.

Understanding what your policy covers and what it excludes sets the foundation for making informed decisions about additional protection. The next section examines the specific coverage options available to Texas landlords and how to select limits that match your property’s actual exposure.

Core Coverage You Actually Need

Dwelling Coverage: The Foundation of Your Protection

Dwelling coverage forms the backbone of any landlord policy in Texas, and selecting the right limit prevents financial devastation. This coverage pays to repair or rebuild the structure itself after fire, wind, hail, theft, or vandalism-the perils that destroy rental income fastest. A property valued at $200,000 typically requires dwelling coverage around $250,000 to account for inflation and rebuilding costs, which translates to annual premiums between $1,800 and $2,500 depending on location and property condition.

Most landlords make a critical mistake by selecting coverage limits based on what they paid for the property rather than what it costs to rebuild today. Replacement cost coverage matters far more than actual cash value because it pays full reconstruction expenses without depreciation deductions, protecting you from absorbing thousands in out-of-pocket costs after a loss.

Protecting Additional Structures and Personal Property

Other structures coverage extends protection to detached garages, storage sheds, or guest houses on your property-typically covering 10 percent of your dwelling limit automatically, though you can increase this if needed. Personal property coverage protects appliances, furnishings, and maintenance equipment you own inside rental units, but this does not cover tenant belongings, which tenants must insure themselves through renters insurance.

Liability Coverage: Your Financial Shield

Liability coverage separates landlords who stay solvent from those facing catastrophic claims. Standard liability limits of $300,000 to $1,000,000 protect you when someone is injured on your property and pursues legal action, covering medical bills, legal defense costs, and settlement amounts. Medical payments coverage, typically $5,000 to $10,000, covers small medical bills regardless of fault-useful when a tenant’s guest trips on the porch and needs emergency care.

Texas properties experience significant liability exposure because injury claims can arise from tenant accidents, guest injuries, or even conditions you did not directly cause but are held responsible for under premises liability law. Umbrella policies add an extra $1,000,000 or more in liability protection above your standard policy limits, costing roughly $150 to $300 annually and providing essential protection for high-value properties or portfolios with multiple units.

Loss of Rent and Additional Living Expenses

Loss of rent coverage provides financial protection against risks such as tenant-caused damage, natural disasters, or liability claims for your rental property. For a property generating $1,500 monthly rent, you should try to select coverage that reflects at least three to six months of lost income to account for extended repair timelines after major damage.

Additional living expenses coverage pays temporary housing costs if you must occupy the property yourself during repairs, though this applies primarily to owner-occupied rentals rather than pure investment properties. The specific coverage limits you select directly impact your ability to recover financially after a loss, which makes the next section-understanding how to avoid common mistakes-essential to protecting your investment.

Common Mistakes Texas Landlords Make with Insurance

Selecting Dwelling Coverage Based on Purchase Price

Most Texas landlords severely underestimate replacement costs and select dwelling coverage limits based on what they paid for the property rather than what it actually costs to rebuild today. A property you bought for $180,000 five years ago may cost $250,000 to rebuild due to labor and material inflation, yet landlords routinely cap coverage at their original purchase price. When a fire destroys the structure, the insurer pays only what you selected as your limit, leaving you to cover the gap from your own pocket. This mistake costs property owners tens of thousands in unrecovered losses. The Texas Department of Insurance does not mandate specific coverage amounts, which creates a false sense that you can choose whatever limit feels comfortable, but comfort and adequate protection are not the same thing. Request a replacement cost estimate from a local contractor before finalizing your dwelling coverage limit, then add 10 to 15 percent as a buffer for cost increases during actual reconstruction.

Underestimating Liability Exposure and Skipping Umbrella Coverage

Equally damaging is underestimating liability exposure or skipping umbrella coverage entirely. A tenant’s guest slips on your property, suffers a serious injury, and sues for $500,000 in damages, but your policy only carries $300,000 in liability coverage, leaving you personally responsible for the $200,000 shortfall. Texas courts do not cap premises liability awards, meaning injury claims can easily exceed standard policy limits, especially if negligence findings are clear. Umbrella policies add an extra $1,000,000 or more in liability protection above your standard policy limits at a cost of roughly $150 to $300 annually, providing essential protection for high-value properties or portfolios with multiple units.

Failing to Update Coverage After Property Changes

Property improvements change your coverage needs, yet many landlords file these changes away without contacting their insurance agent. You add a pool to the rental property, but your policy still reflects coverage for a property without one, leaving that new liability exposure completely uninsured. Renovations to the kitchen, additions of a deck, or upgrades to electrical systems all change your property’s risk profile and replacement cost. Your policy becomes outdated within months of any meaningful improvement, creating gaps that surface only when you need to file a claim. Contact your insurance agent annually to review whether your coverage still matches your property’s current condition and value, especially after any improvements or structural changes.

Final Thoughts

Protecting your Texas rental property requires more than hoping nothing goes wrong. Landlord insurance in Texas addresses the specific risks you face as a property owner, from hurricane damage on the coast to liability claims in urban markets. The mistakes covered in this guide-underinsuring your dwelling, skipping liability protection, and ignoring coverage updates-cost landlords real money when claims happen.

We at Brooks Cannon Insurance Group work with multiple top-rated insurance carriers to find coverage that matches your property’s actual exposure and your financial situation. As an independent agency based in Dallas, we understand the regional risks that affect rental properties across Texas, from coastal flood zones to urban liability concentrations. Our licensed experts review your coverage annually to catch gaps before they become expensive problems.

Contact Brooks Cannon Insurance Group to discuss your current coverage or get quotes on a new policy. Bring details about your property-its age, location, value, and any recent improvements-so we can recommend appropriate limits and identify available discounts. A thorough review takes an hour and can save thousands when a loss occurs.