Construction projects in the Dallas area face real financial risks. One accident or property damage claim can derail your entire operation and drain your finances.

Builders risk liability insurance protects you from these costly scenarios. At Brooks Cannon Insurance Group, we help contractors understand exactly what coverage they need and how to get it in place before work begins.

What Builders Risk Liability Insurance Actually Covers

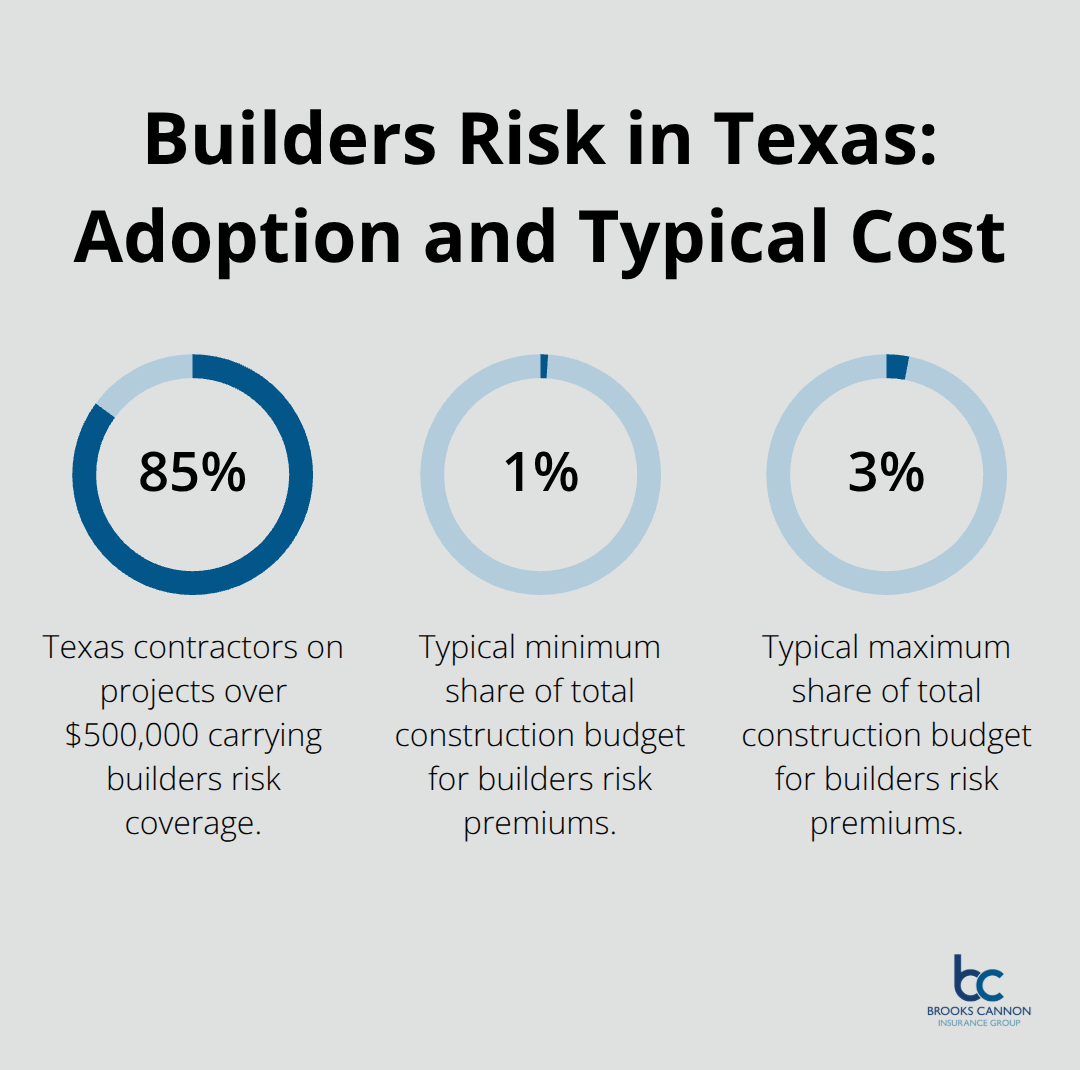

Builders risk liability insurance is not one policy-it’s two separate protections that work together on construction sites. The first part covers physical damage to the building, materials, equipment, and temporary structures like scaffolding and fencing. The second part covers bodily injury and property damage claims from third parties injured on your job site. This distinction matters because standard commercial policies exclude coverage for buildings under construction, leaving you exposed during the phase when your project is most vulnerable. In Texas, where 85% of contractors working on projects over $500,000 carry this coverage according to the Associated General Contractors of America, the insurance typically costs between 1% and 3% of your total construction budget. For a $500,000 project, that translates to $5,000 to $15,000 in annual premiums-a manageable expense compared to the financial devastation of an uninsured loss.

What the Property Damage Section Actually Protects

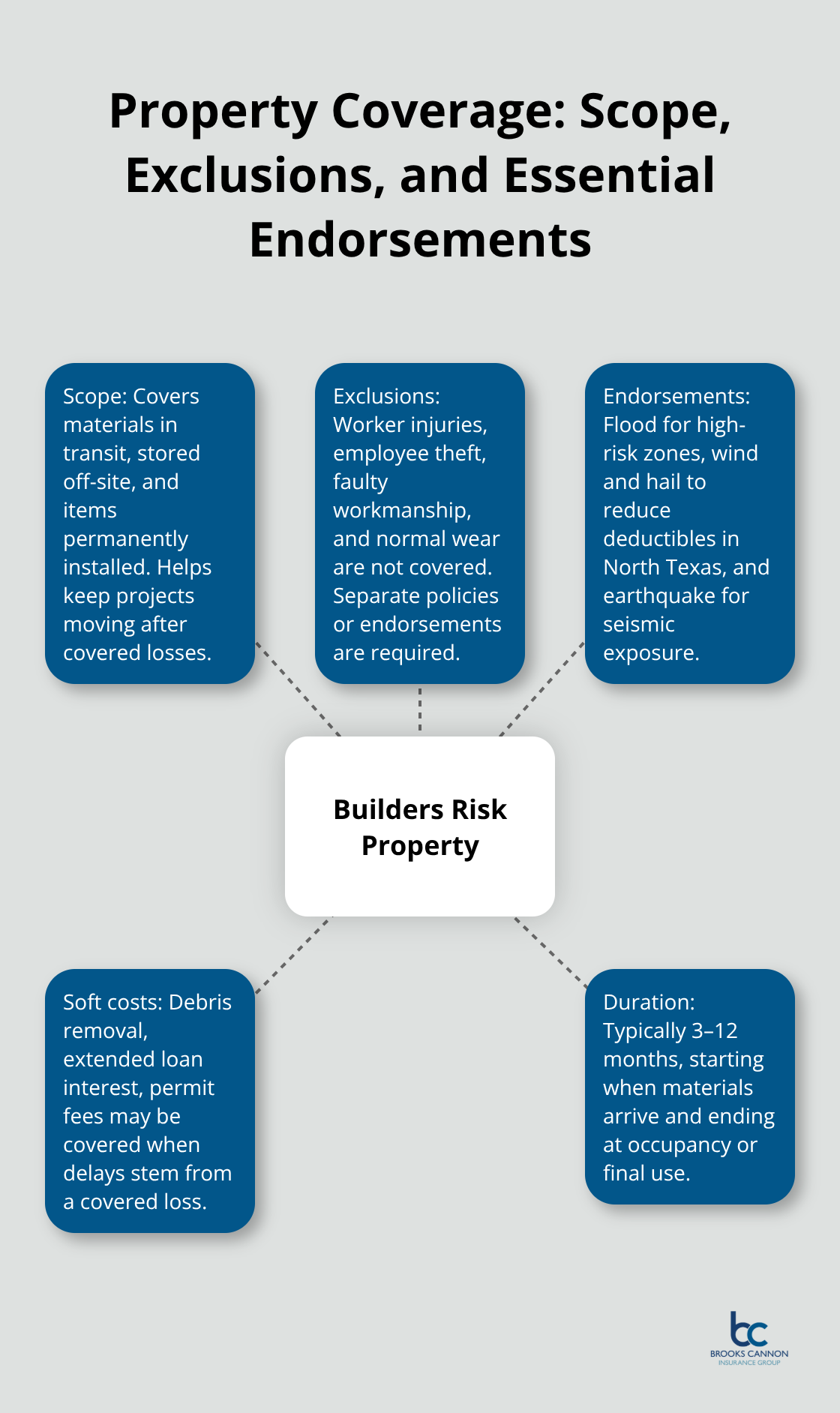

The property damage portion covers fire, wind, hail, theft and vandalism, and water damage from burst pipes or leaks. In North Texas, hail damage is particularly relevant since the region sits in Hail Alley, where over 2 million Texas homes were affected by hailstorms in 2023, causing record-breaking insured losses during construction. Coverage extends to materials in transit, stored off-site, and items permanently installed. Debris removal and soft costs like extended loan interest and permit fees qualify for coverage when delays result from a covered loss. However, standard policies exclude worker injuries (you need workers’ compensation for that), employee theft, faulty workmanship, and normal wear. Endorsements fill critical gaps-flood coverage matters for projects in high-risk zones, wind and hail endorsements reduce deductibles in North Texas, and earthquake coverage protects against seismic events.

The policy duration typically runs 3 to 12 months depending on project size, beginning when materials arrive and ending at occupancy or final use.

Who Actually Needs This Coverage and Why

Contractors, property owners, developers, and lenders all need builders risk liability insurance because financial interest in the project creates legal responsibility. Most construction lenders require proof of coverage before releasing funds-they’re protecting their investment in your project. Subcontractors typically appear as additional insureds on the main policy, though contracts should specify who carries the primary coverage to prevent gaps. The liability portion is equally critical because a single slip-and-fall claim can exceed $100,000 in medical costs and legal fees. Standard builders risk excludes premises liability claims, meaning you need separate general liability coverage to protect against third-party bodily injury. This combination of property and liability protection is non-negotiable in Dallas and surrounding areas where construction activity is constant and weather-related claims are routine.

How Timing Affects Your Coverage Options

You should obtain quotes from multiple carriers at least 30 days before your project starts-most brokers can deliver quotes within 24 hours and bind coverage in 48 hours or less for standard projects. Starting this process early prevents last-minute gaps that leave your materials and workers unprotected. Lenders often refuse to release construction funds without proof of active coverage, so timing your application correctly keeps your project on schedule. If construction delays occur, you can extend your policy to match the new completion date, but you must contact your broker at least 30 days before expiration to arrange the extension.

How to Assess Your Coverage Needs

Calculate Your Total Project Cost Accurately

Your project’s total cost directly determines your coverage limits, and underestimating this number leaves you financially exposed. A $500,000 residential renovation requires different protection than a $2.5 million commercial build, yet many contractors apply a one-size-fits-all approach that fails when claims exceed their policy limits. Start by calculating your total construction budget including labor, materials, fixtures, equipment, and temporary structures like scaffolding and fencing. For Dallas-area projects, the Associated General Contractors of America reports that 85% of contractors on projects exceeding $500,000 carry builders risk coverage, which typically costs 1% to 5% of your total construction budget. This means a $500,000 project runs $5,000 to $25,000 annually, while a $2.5 million project costs $25,000 to $125,000. Your coverage limit should match or exceed your total project value to prevent gaps.

Account for Construction Type and Duration

North Texas construction types matter significantly-frame structures cost more to insure than fire-resistant masonry because wood framing presents higher loss exposure to hail and wind. Project duration affects pricing too; a three-month renovation costs less than a twelve-month commercial build because your materials remain at risk longer. If your project spans multiple locations or involves materials moving between job sites, inland marine coverage fills gaps that standard builders risk excludes, protecting tools and equipment in transit.

Identify Location-Specific Risks and Required Endorsements

Your specific location in the Dallas area determines which endorsements you absolutely must purchase rather than treating them as optional upgrades. North Texas sits in Hail Alley, where hailstorms caused record insured losses in 2023 affecting millions of properties, so wind and hail endorsements with reduced deductibles become essential rather than nice-to-have additions. Flood coverage is mandatory for projects in high-risk zones near the Trinity River or in areas with poor drainage history-standard policies exclude flood damage entirely. Coastal projects require windstorm coverage because hurricane exposure increases premiums significantly compared to inland locations.

Protect Materials and Address Hidden Costs

Theft and vandalism coverage protects materials on-site, in transit, and in temporary storage, though employee theft remains excluded and requires a separate crime policy. Debris removal coverage handles cleanup costs and regulatory compliance expenses after a covered loss, preventing unexpected out-of-pocket expenses. Soft costs coverage protects extended loan interest, permit fees, and architectural charges when construction delays result from a covered event like fire or severe weather.

Review Contract Requirements and Lender Demands

Document your specific risks by reviewing your construction contract requirements, your lender’s insurance demands, and your subcontractors’ coverage needs. Most lenders require proof of coverage before releasing funds, and they specify minimum limits you must maintain throughout the project. Once you understand your coverage needs, the next step involves gathering the documentation that carriers require to issue quotes and bind your policy.

Steps to Obtain Builders Risk Liability Insurance

Prepare Your Documentation Before Contacting Carriers

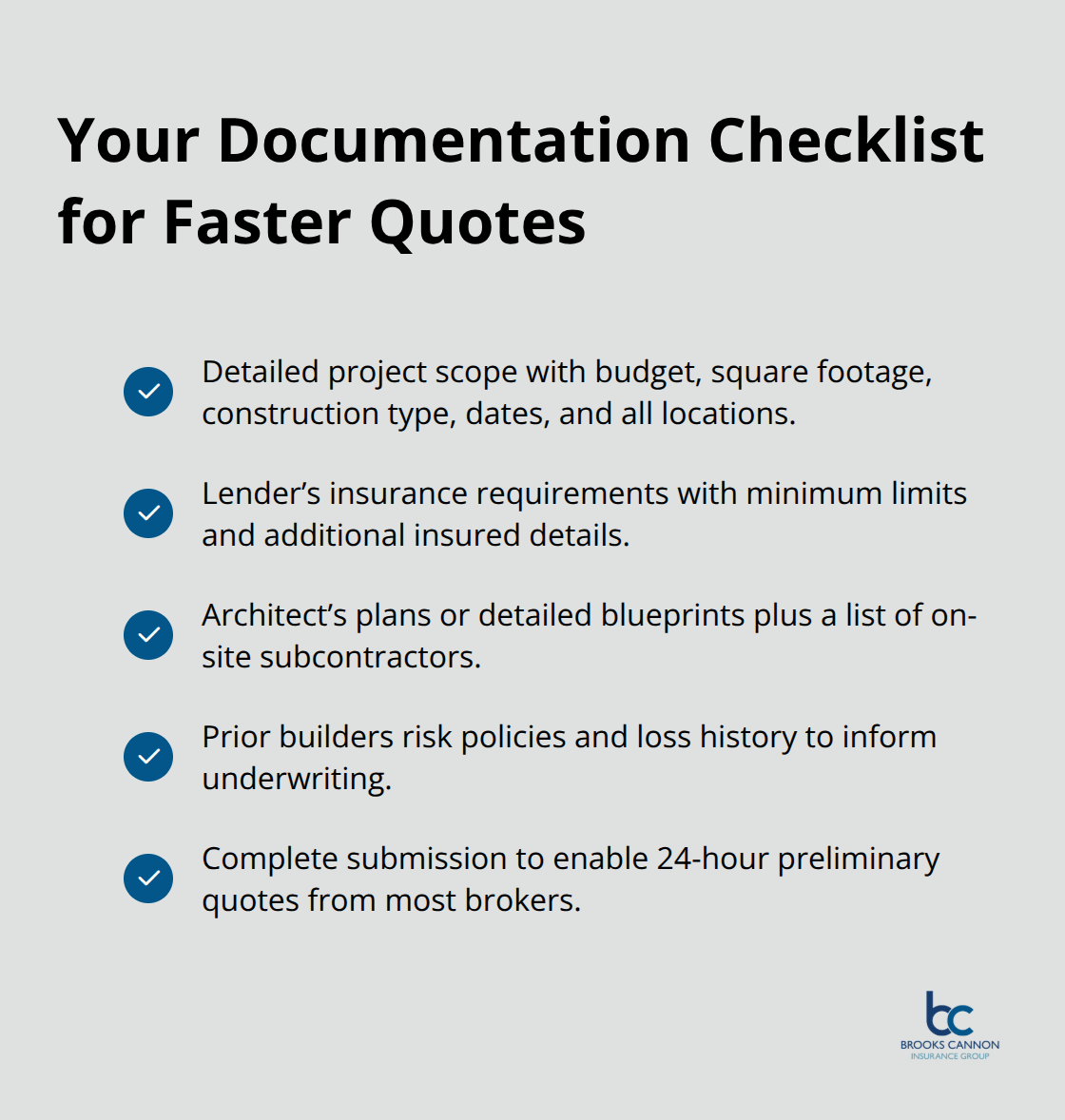

Carriers require specific information to issue accurate quotes, and you save days of delays by preparing this documentation upfront. Compile your detailed project scope, which includes the total construction budget, square footage, construction type (frame versus masonry), project start and completion dates, and a list of all locations where work will occur. Pull your lender’s insurance requirements from your financing agreement because carriers must verify that your policy meets your lender’s minimum limits and additional insured requirements.

For Dallas-area projects, have your architect’s plans or detailed blueprints ready, plus a list of subcontractors who will work on-site. The more complete your initial submission, the faster carriers issue firm quotes. Most brokers deliver preliminary quotes within 24 hours once they receive this information, but incomplete submissions stretch that timeline to 3-5 days. If you’ve carried builders risk coverage before, locate your previous policies-loss history directly impacts your premium, and carriers want to see your claims record upfront.

Request Quotes Using Identical Coverage Parameters

Comparing quotes from multiple carriers reveals dramatic price variations for identical coverage. Most Dallas-area brokers access 80+ carriers through their underwriting platforms, which means working with a single agent gives you access to far more options than approaching carriers directly. Request quotes using the same coverage limits and deductibles across all carriers so you compare apples to apples; a $5,000 deductible policy from one carrier costs significantly less than a $1,000 deductible from another, but that savings disappears when you file a claim. Pay attention to how carriers handle endorsements-some bundle wind and hail coverage into the base premium for North Texas projects, while others charge it as an add-on, making their quoted price artificially low.

Evaluate Carrier Service Quality and Local Presence

Ask each carrier specifically about their claims process, response time, and whether they have local adjusters in the Dallas area; a cheap premium means nothing if the carrier takes six weeks to respond to your theft claim. Carriers with established local presence in Texas typically understand North Texas weather risks and process claims faster than national carriers unfamiliar with regional loss patterns. Once you narrow your choices to two or three carriers with competitive pricing and strong local service records, work with an independent agent to finalize coverage before your project materials arrive on-site.

Final Thoughts

Builders risk liability insurance protects your Dallas-area construction projects from the financial devastation that comes with property damage, theft, or third-party injury claims. The coverage you need depends directly on your project size, location, construction type, and the specific risks your site faces. A $500,000 project in North Texas requires different protection than a $2.5 million commercial build, and skipping endorsements like wind and hail coverage in Hail Alley leaves you dangerously exposed when storms hit.

Lenders won’t release construction funds without proof of active policies, and a single uninsured loss can bankrupt your operation. The 85% of Dallas-area contractors carrying builders risk on projects over $500,000 understand that the 1% to 3% annual premium cost is trivial compared to the financial exposure they face. Timing your application correctly prevents gaps that leave your materials unprotected, and requesting quotes from multiple carriers reveals pricing variations that can save thousands of dollars annually.

Contact Brooks Cannon Insurance Group today to discuss your builders risk liability insurance needs. We work with multiple top-rated carriers to find the coverage and pricing that matches your specific project needs. Our team understands North Texas weather risks, lender requirements, and the documentation carriers demand, which means we deliver accurate quotes faster and bind coverage before your materials arrive on-site.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation